Bretton Woods Is No Mystery and The Nixon Shock

Posted: March 7, 2021 Filed under: America Since 1945, business, money, New England Leave a commentBreaking the Breton Woods agreements, the American president said that the dollar would have no reference to reality, and that its value would henceforth be decided by an act of language, not by correspondence to a standard or to an economic referent.

That’s from The Uprising: On Poetry and Finance, by Italian communist Franco “Bifo” Berardi, published by semiotext(e). Full of interesting ideas.

Everywhere I turn these days, from the new Adam Curtis documentary to the Bitcoin-heads on Twitter, I hear about Sunday, August 15, 1971. On that evening, Richard Nixon, conferring with his advisors in a weird weekend at Camp David, went on TV and announced he was taking the US dollar off the gold standard. Nixon ended the “Bretton Woods system.”

Always had an interest in the Bretton Woods system. Worked out at the Mount Washington Hotel in Bretton Woods*, New Hampshire. My dad and I went cross-country skiing up there.

The hotel shut up for winter had a spooky, imposing quality.

President Franklin Roosevelt proposed the conference site, the Mount Washington Hotel, as a ploy (successful, as it turned out) to win over a likely opponent of the pact, New Hampshire senator Charles Tobey.

That’s from Michael A. Martorelli’s review of Benn Steil’s book about the conference, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order.

The conference happened in July 1944. The Allied forces were stalled in the bocage of Normandy. But leadership was planning for the postwar order. John Maynard Keynes, who’d studied the disaster of the last postwar peace, was trying to avoid the same mistakes while attempting to save the dignity of the UK. Keynes suggested the world switch to a global currency called Bancor. The US, represented by Harry Dexter White, dominant, had the strong position. The US proposed to leave the US dollar, pegged to gold, as the world’s reserve currency.

Deeply indebted to the United States after the long, costly ordeal of World War II, the United Kingdom inevitably lost the battle. To secure one key victory, however, White had to resort to stealth. In the waning hours of the conference, he and his assistants replaced the phrase “gold” with “gold and US dollars” in the agreement, thereby enshrining the US currency as the international medium of exchange. Keynes confessed that he did not read the final version of the document he signed.

You think there aren’t thrills in a book about a 1944 economic conference whose results have been overturned? Wrong:

In one noteworthy coup, [Steil] disproves Keynes biographer Robert Skidelsky’s claim that Keynes was assigned Room 129 in the Mount Washington Hotel.

The summit does sound exciting. The Soviets brought a bunch of female “typists” to seduce everyone.

One committee of delegates took a 15-minute recess in the bar each night at 1:30 to watch the “titillating gyrations of Conchita the Peruvian Bombshell.” Afterward, reinvigorated, they would negotiate for another hour or so. The long arguments left White increasingly short-tempered on less than five hours of sleep a night. Keynes, already weakened by the heart disease that would kill him within two years, was soon holding court from his bed, tended (and guarded) by Lydia, his eccentric Russian ballerina wife. At one point, a rumor spread that he was near death; when he then appeared at dinner, the delegates spontaneously stood and sang “For He’s a Jolly Good Fellow.”

from a different review of a different book about the conference:

I’ve taken a look at both Steil and Conway’s books. The Summit by Conway is more fun and easy to read, and focuses on the wild details – what he calls the “noises off” stuff – from the conference. The drunken songs, the parody newspaper about the “International Ballyhoo Fun,” the pleasure delegates from wartorn countries took in plates of “chicken Maryland” and bowls of ice cream, the South Africans playing golf once it was clear gold wouldn’t be replaced by silver, the results of the Soviet vs USA volleyball game (USSR won), that’s in Conway.

The details of the conference are interesting, but the outcome was inevitable. The US was the last power standing as World War II ended. The UK was in our debt (literally). What we ended up with was the system we devised: the dollar as default world currency.

The true significance of the conference was noted by Keynes in a speech at the farewell dinner:

We have shown that a concourse of 44 nations are actually able to work together at a constructive task in amity and unbroken concord. Few believed it possible. If we can continue in a larger task as we have begun in this limited task, there is hope for the world.

If you read one review of one book about the conference, read James Grant’s review of Steil in the Wall Street J (behind a paywall, they’re no fools about money at the WSJ):

Gold figures largely in these pages. The ancient metal was deeply rooted in the psyche of Keynes’s contemporaries, including that of Lt. Col. Sir Thomas Moore, a British Conservative member of Parliament. In parliamentary debate, Sir Thomas said that he had “the impression, not being an economist, that currency had to be tied to or based on something; whether it was gold, or marbles, or shrimps, did not seem to matter very much, except that as marbles are easy to make, and shrimps are easy to catch, gold for many reasons possessed a more stable quality.” For the soundest doctrine expressed in the fewest words, Sir Thomas was hard to beat.

Grant, if you can’t read it, isn’t too boosterish on the Bretton Woods system:

Rare among nations, America pays its overseas debts in money that it alone may lawfully print. Naturally, being human, we Americans have printed to excess. Not since 1975 has the United States exported more goods and services than it has imported. There is no institutional check to square up accounts. We buy Chinese merchandise with dollars. The Chinese, in turn, invest those dollars in U.S. government securities (the better to suppress the value of the Chinese currency). It’s as if the money never left the 50 states. In possession of the “reserve currency” franchise—White’s dream fulfilled—America has become the world’s leading debtor nation. At Bretton Woods, it was the world’s top creditor.

Mentioned the Nixon Shock to a bud who works at a hedge fund, and he put me on to WTF Happened in 1971, which takes a darker view. Love the idea that this is the moment everything went wrong and reality broke, but I’m not convinced. What about the Triffin dilemma? Was Nixon changing reality, or acknowledging it?

Consider how things worked before Bretton Woods. Both Conway and Stiel note that FDR would dictate the dollar price of gold from bed in the morning, once raising the price by twenty-one cents because that was a lucky number. This was more “real”?

A crazy element of the conference is that the leader of the US delegation, Harry Dexter White, was communicating with the Soviets. To what extent he was a traitor, a spy, vs kind of backchannel with our wartime ally is unclear. But declassified transcripts make clear he was a Soviet asset known at “Jurist” or “Richard.” That’s if you trust our own NSA. Who knows?

White testified in front of HUAC that he was not a Communist, then had a heart attack. He went to his home in New Hampshire and died four days later.

Is it possible White sabotaged the US team in the Bretton Woods volleyball game? To provide a propaganda win for his Soviet masters? The Russians got a lot of concessions at Bretton Woods to induce them to sign on to the agreements. But I don’t see in Steil or Conway any case that White’s possible connection helped them. Conway is a skeptic on the spy stuff, suggesting that yes, it looks fishy, but it’s impossible to prove White “betrayed his country.”

One person who would’ve known White had been a spy? President Richard Nixon.

Following Alger Hiss’s perjury conviction in 1950, Representative Richard M. Nixon revealed a handwritten memo of White’s given to him by Chambers, apparently showing that White had passed classified information for transmission to the Soviets. Yet his guilt would only be firmly established after publication of Soviet intelligence cables in the late 1990s.

The IMF and World Bank linger as Bretton Woods legacies. Conway in his epilogue notes how even after the demise of the Bretton Woods system, the IMF still imposes the “Washington Consensus” on the developing world in return for loans. Maybe someone should activate the Coconut Clause:

Conway also notes that after the demise of the system, US and British banks became more profitable.

In the United States, by the turn of the millennium banks now accounted for around 8 per cent of the country’s total economic output – more than double their zie when the Bretton Woods system ended… Until 1970, an investor in a UK bank could expect to make about 7 per cent a year on his investment. After 1970, the return on equity roughly trebled to 20 per cent, a figure maintained without a break until the financial crisis of 2008.

There is no single, simple explanation for this astonishing rise of the financial sector; however, there is no doubt that one important element is the sudden change in the international monetary architecture following the collapse of Bretton Woods. Almost immediately after the demise of Keynes and White’s system in the early 1970s, every single measure of the size, profitability, and leverage of the banking industry has begun to increase at unprecedented rates.

The big banks in the USA tried to stop Bretton Woods at the time,

After the Bretton Woods conference, the countries involved had to sell it to a confused public. One method the USA used was a pamphlet called Bretton Woods Is No Mystery, illustrated by the New Yorker cartoonist Syd Hoff. I’m on the trail of a copy, I can only find a few images online.

Heartbreaking to hear the names bandied about for the world currency, and think what might’ve been. From Conway:

among the suggestions were Fint, Proudof, Unibanks, Bit, Pondol, and Keynes’ favorite, Orb. Months later, Keynes sent round a note to his Treasury colleagues asking: “Do you think it is any use to try unicorn on Harry?”

What do you guys think will be the world’s reserve currency in 2031? Dogecoin?

*an archaic name for what’s now part of Carroll, New Hampshire.

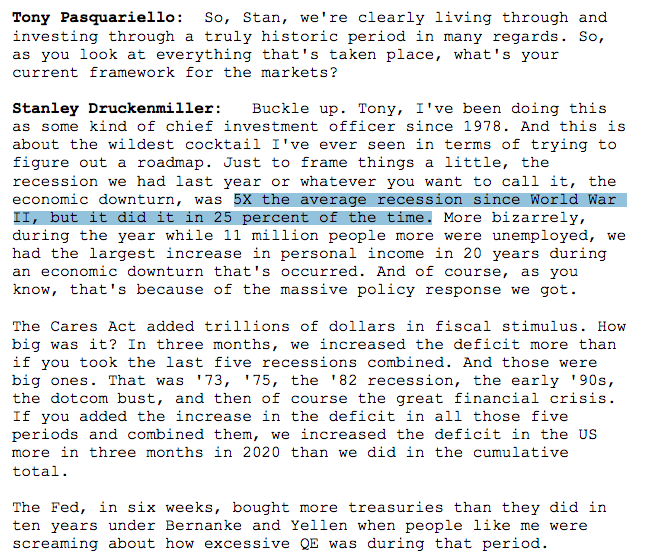

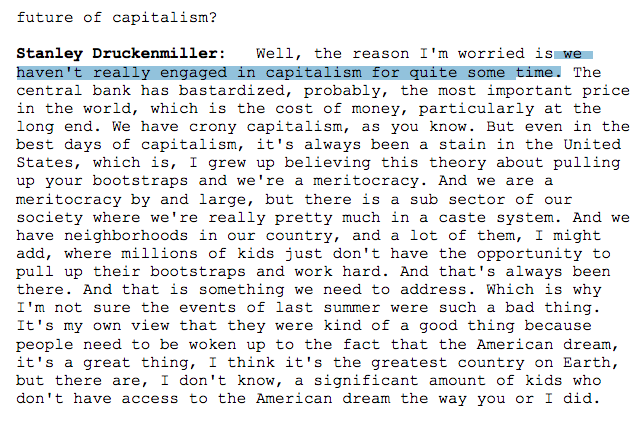

Buckle up Tony

Posted: March 1, 2021 Filed under: America Since 1945, business 1 Comment

from this Talks at Goldman Sachs discussion with Stanley Druckenmiller. How about this?:

Let’s clear the desktop screenshots

Posted: February 28, 2021 Filed under: America Since 1945 Leave a comment

good guess Facebook.

re: the Trump golden statue. From Politico Playbook. If politics is pro wrestling, Playbook is the closest thing I can find to a “dirt sheet.”

incredible. Wall Street J. Great newspaper, opinion page is absolutely deranged.

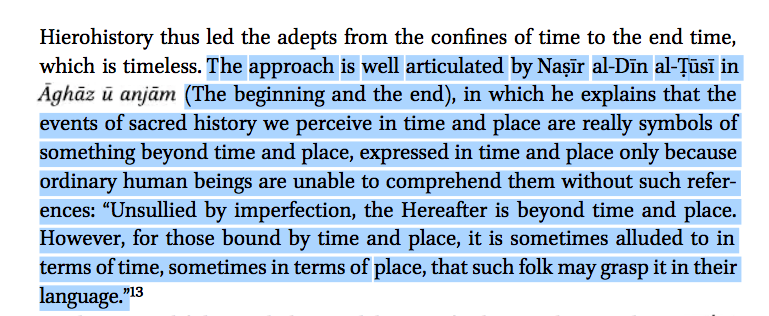

some Shiite theology of the 13th century. from a paper by Shafique N. Virani, Hierohistory in “Qādî-I-Numan’s Foundation of Symbolic Interpretation (Asas al-Ta’wil): the birth of Jesus. ” I was trying to learn more about al-Tusi saving 200,000 books from the House of Wisdom and brought them to Maragheh and as usual got more than I bargained for.

somewhat grim headline in Bloomberg. If I had all the time in the world I might compose a history and exploration of the meanings and suggestions of the phrase “want fries with that?” My conclusion would be “French” fries are distinctly American, that “fry culture” is both good and bad, reflecting both our mobility and freedom and some our shortcomings, and that the economics of fries represent both the best of the capitalist system (cheap tasty calories distributed with efficiency) and the worst (exploitative labor system, nasty and unpriced effects on health and environment).

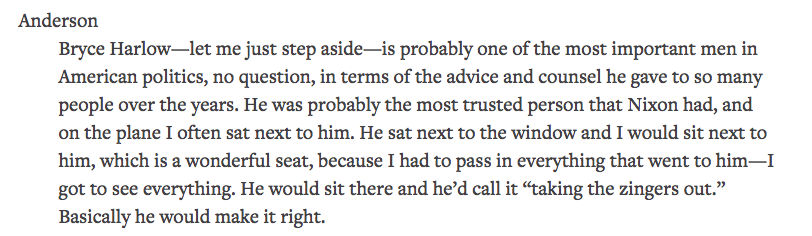

from a Martin Anderson oral history over at the Miller Center. Anderson was an aide to Reagan and wrote a very illuminating book on the man and the movement, one of the most revealing books on Reagan, in my opinion: Revolution. He’s a believer.

Scott Carpenter

Posted: February 28, 2021 Filed under: America Since 1945 Leave a comment

“I volunteered for a number of reasons,” he wrote in “We Seven,” a book of reflections by the original astronauts published in 1962. “One of these, quite frankly, was that I thought this was a chance for immortality. Pioneering in space was something I would willingly give my life for.”

(photo from NY Times / Associated Press)

The grass is always greener

Posted: February 28, 2021 Filed under: America Since 1945, presidents 2 Comments

Reagan not only had the sense of humor, the great jokes. I remember one time in the Oval Office he was looking out and there was a bunch of people chopping things and the forest rangers standing out on the South Lawn, and Clark says, Mr. President, Ken’s here to take you to the Situation Room or something. We were getting ready for the next round or summit or whatever it was. Reagan keeps looking out and this sound gets louder and he says, I hear you, Bill. Just wish I was doing what those fellows are doing instead of going to all these stupid meetings hours at a time.

I thought to myself, in the history of the United States, 200 years, we’ve had forest rangers who imagined themselves as President, but I can’t imagine a President imagining himself as a forest ranger before. Here he was, dying to be a forest ranger. Reagan was like that.

from an oral history with Reagan Arms Control and Disarmament Agency head Ken Adelman at the Miller Center.

This reminded me of when I’d be sitting in my office on the 11th floor above the Ed Sullivan Theater grinding out some comedy for The Late Show with David Letterman, a cushy if psychologically taxing job, and find myself staring out the window and fantasizing about being a guy on one of the tugboats going up the Hudson.

Adelman seems to suggest this idea was unique to Reagan, but I bet almost every president has felt this way at one time or another. Although maybe not, maybe Nixon or LBJ would’ve been sick at the idea of falling to the state of a powerless treecutter.

from the tailings

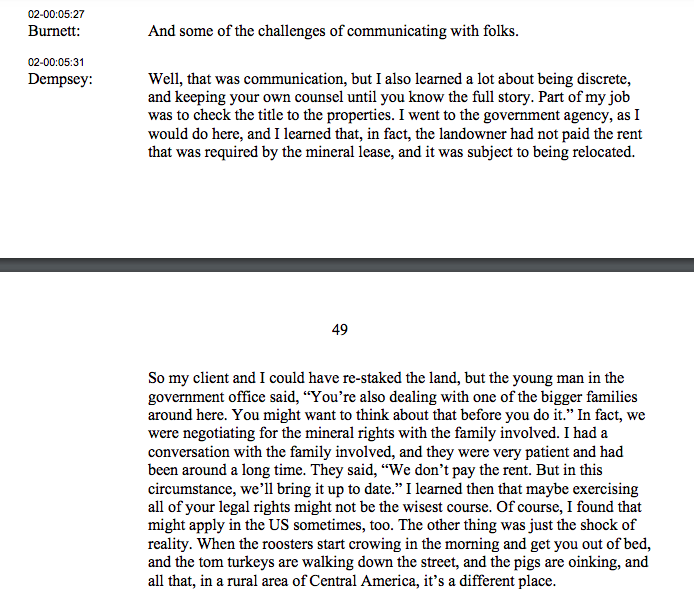

Posted: February 23, 2021 Filed under: adventures, America Since 1945, mining Leave a commentOne thing led to another and I read a long oral history with mining entrepreneur Stanley Dempsey. Here are some li’l nuggets of mild interest. On pursuing claims in Nicaragua:

on the mining boom towns of Colorado:

Sometimes, not being an expert is an advantage:

The 1872 Mining Law, which creates self-initiated rights, kind of unique to the United States, seems very important to this country’s development.

Have you heard of this man?

Posted: February 11, 2021 Filed under: America Since 1945 Leave a comment

That is Walter Hines Page. In the 1920s, two different Pulitzer Prizes in biography were awarded for books about him. He was a writer, editor, and publisher, his main historical distinction seems to have been helping bring the USA into World War I:

Page was appointed U.S. ambassador to the United Kingdom by President Woodrow Wilson, whom Page had befriended in 1882 when Wilson was a young lawyer starting out in Atlanta. Page was one of the key figures involved in bringing the United States into World War I on the Allied side. A proud Southerner, he admired his British roots and believed that the United Kingdom was fighting a war for democracy. As ambassador to Britain, he defended British policies to Wilson and helped to shape a pro-Allied slant in the President and in the United States as a whole. One month after Page sent a message to Wilson, the U.S. Congress declared war on Germany.

So far in the 2020s the only subject for a Pulitzer Prize-winning biography has been Susan Sontag.

Winning a storytelling contest

Posted: January 29, 2021 Filed under: America Since 1945, business Leave a comment

One reason to be interested in the stock market is it can become a storytelling contest. Take the story of GameStop. There was a prevailing story, a sad story, that GameStop was Blockbuster all over again. Old mall stores, a dying dinosaur selling product that’s now online.

But then, people stood up and said, that’s not the story of GameStop. The story of GameStop is that yeah, it might need to change, but it’s not dying. It’s healthy. GameStop can live a long time. What’s more, it has real advantages, it just demonstrated some of them last Christmas. With clever thinking and fast action GameStop could succeed. It could even be big.

Then, in a place where people gather and share stories, an even more riveting story arose. A bunch of cocky suits have made arrogant bets on the old story of GameStop. They’re planning to feast on the carcass, as if they don’t have enough to feast on. But guess what. They’re not as smart as they think. There’s something they didn’t plan on. They wrote a check their ass can’t cash. If someone calls ’em on it? They’ll be ruined.

The power of this story became so strong that by now everyone’s heard it. Robinhood (and what story are they trying to tell? You’re out here saying you’re as good as Robin Hood?! Robin Hood, played by Errol Flynn, a Disney fox, Kevin Costner, and Picard?!) whose ball everyone was using had to declare a sudden rule change. Which every child knows is bullshit behavior and unfair.

Is that story true? Does it matter?

At some level there is truth to be faced. There are debts with dates on them and courts and legal power that will enforce them. But the value of GameStop, we’ve now seen, is a story that can be changed very quickly by compelling storytellers. The idea that the correct story is somehow already embedded in the stock price has been proven many times to not always be the case, no matter how many Sveriges Riksbank Prizes in Economic Sciences in Memory of Alfred Nobel are given suggesting such. (Note who gives that prize, by the way: a central bank, which has a vested interest, in fact its only interest, in maintaining a a steady, stable, version of the story of economics).

Sverges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel winner Robert Schiller didn’t miss this, he wrote a book about the power of stories:

(I’m working my way through it).

Oh and by the way money itself is a kind of story. Ever since 1971 when Nixon took the US dollar off the gold standard, money “floats,” money is an act of language, money is based on the story that the US government will honor the words on paper dollars and accept those for debts (which are themselves stories).

So, where does that leave us?

No idea, I’m riveted by the story. Who would add a jot to the GameStop discourse, it’s overwhelming! I can’t even keep up with Matt Levine, a great storyteller about these matters.

change / the same

Posted: January 27, 2021 Filed under: America Since 1945, business, New England 1 Comment

That’s Van Wyck Brooks, going off in The Flowering of New England about the generation of the 1840s.

funny way to summarize the plot of Wind-Up Bird Chronicle

Posted: January 27, 2021 Filed under: America Since 1945, business Leave a comment

That’s from:

the gist of which is that Oprah, Bill Gates, Sheryl Sandberg, and Whole Foods’ John Mackey sort of perpetuate a new version of the capitalist gospel rather than advocate for real or systemic change. But, you already knew that, didn’t you? Would it be more worthwhile to explore why stories of hustle and self-determination and drive remain so appealing to people despite the seeming fact that we’re trapped by oppressive and exploitative systems full of unfairness? Maybe that’s art’s job, not sociology’s.

The stock market is pretend until it isn’t

Posted: January 25, 2021 Filed under: America Since 1945, business Leave a commentSometimes, calls get called. When the stock market becomes real, it becomes very real.

Consider the naked short, explained in this medium post, “GameStop: Power To The Market Players,” by Nope, It’s Lily:

If you’ve been anywhere in the trading universe, it’s been partly a meme and partly a higher calling to long $GME since about July/August 2020, when everyone suddenly realized the short interest on $GME actually exceeded its available float. In English, this meant that there were more shares sold short (a strategy to benefit from the stock price going down, this involves borrowing a share to sell with the intent to repurchase it at a lower cost later) than actually available to buy. How does this happen exactly?

This can happen one of two ways:

Naked shorting — This is a mostly illegal practice in which an individual or institution first sells shares without locating that they well, actually exist. This is fairly sneaky, but works as long as they can find the shares before the settlement period (delivery date) of the shares actually occurs. If they find it before then, no one is the wiser (except the SEC, when it decides to do anything ever).

Despite what idiots online believe, naked shorting isn’t always illegal (hence the word mostly). In particular, the ban on naked short-selling (Regulation SHO) isn’t because the government thinks you’re a meanie for doing it, but because of its hypothesized connections to the 2008 financial crash (actual data on it is mixed). In general, the belief was that naked short sellers helped destabilize investor confidence in the banks, leading to that fun period best remember by watching The Big Short accompanied by a full handle of Svedka.

Naked shorting, however, is legal by bona-fide market makers, which according to our SEC friends means simply it is done to hedge an option position sold (as part of market making duties, to buy and sell a security at publicly stated prices) rather than for speculation. If you want to read boring legal stuff, here’s a link to Regulation SHO.

Similarly, despite what your favorite rocket-emoji’ing internet guru believes, causing an actual short squeeze is hard, and almost always mostly illegal. The last public short interest (the next one should be released on January 27th, per FINRA reporting) on GME was released on Dec 31st, 2020.

Second bold mine.

I can’t say I understand the article. My first experience with this journalist. I’ll be interested to see what happens on January 27th.

The GameStop story is very compelling. Matt Levine’s take as always definitive. Comparisons to what Trump and Trumpians did to the GOP (and then the country) in 2016: an ebullient Internet-centered group of trolls realize there are tricks they can use to mock and demolish the establishment players, moving faster than the other guys can say “hey, what a second, that isn’t how we play!” The end result of that gleeful message board based takeover was (glances at Washington) huh looks like establishment people with 40 plus year careers are back in control of all branches after a brief reign of chaos (though they are rattled by what happened).

Value investing, growth investing, and vibes investing

Posted: January 23, 2021 Filed under: America Since 1945, business Leave a commentor

The Vibes Speculator

You hear about two schools of investing. Value investing, and growth investing. First, value investing.

Value investing involves generating a number for what a company’s intrinsic worth might be, comparing that number to the price the company’s shares are trading for on the stock market, and buying when there’s a discount (plus a margin of safety to account for the risk). You want to buy stocks that are cheap, on sale, and wait for their prices to return to what they should be.

Howard Marks, in his new memo “Something of Value” for Oaktree Capital, has a great definition of value investing, and we’re taking that as our text today. We would quote it extensively, but there’s a stern disclaimer on it. After an email correspondence with Oaktree Capital, I appreciate their denial of my request for permission to use lots of quotes in this piece.

We encourage third parties that are interested in sharing Howard’s memos with an audience to write their own summary/article about the memo and then link to the memo in its entirety on our website. Howard’s memos are meant to be read/viewed in their entirety and removing specific quotes can lead to them being taken out of Howard’s intended context. Also, as we operate in a highly regulated business, we are required to include our legal disclosures to Howard’s writings, and removing portions of his writing without the disclosures attached goes against our internal policies.

as Leia Vincent of Oaktree put it to me in an email. I see their point.

Check out Marks summary of value investing, paragraph four.

investing was pioneered by Benjamin Graham, whose teachings were transcribed by David Dodd, Graham taught Warren Buffett. There’s a lot to love about value investing. It’s bargain hunting. It almost feels virtuous. You must be rational to be a value investor. You must have emotional discipline as the market goes up and down.

Value investing is widely preached. Aswath Damodaran of NYU, who wrote a little book on the topic, will teach you on YouTube. Shawn Badlani spoke about his training as a value investor on episode 8 of my podcast, Stocks: Let’s Talk.

Value investing thinking has served Shawn pretty well. Every investor would be wise to study valuation.

As Marks acknowledges though, value investing has significant downsides. You’ve got to do a lot of calculating of discounted cash flow for one thing. Math, which is maybe not that hard, but tedious. There are computers, which can help you with the math. I like Guru Focus (you gotta pay to be a member) which can do shorthand estimates for you, like this one for Tesla:

but that can only get you so far, and it also reveals another problem. Value investing has imbedded in it both an attraction for the rational and a torture for them: stocks aren’t always trading for what they should be worth.

That is, their price isn’t always what it “should” be. That’s supposed to be an advantage, if you buy them when they’re cheap, and wait for the equilibrium that must come, when their true value will be revealed.

But what if that never happens? Consider the angst of Value Stock Geek, a smart writer on this subject. How long do you wait for the stock to achieve the correct price?

Not only that, but for all that math, you’re still just guessing! All your calculations are only as good as your inputs, some of which are guesses!

Plus, you’re competing against Warren Buffett, Munger, Aswath Damodaran, Shawn, Value Stock Geek, and literally one million other people. Wall Street has been sucking off physicists, computer scientists, “quants” of all kinds, taking them away from useful work and putting them into complex valuation shops. Their computers are faster, more powerful, and more expensive than yours, I guarantee. Their computers blow your puny computer out of the water. They’ve got an Alienware Aurora R11 with Intel Core i9 10900KF and an Nvidia GTX 1650 Super – RTX 3090, with 2TB M.2 PCIe SSD + 2TB SATA HDD and you’ve got an Epson 512K with 5.25 inch floppy disc. Who’s gonna kill if you’re playing Red Baron?

So much for value investing.

Then there’s growth investing.

The story of Marks’ memo is of how spending time during the pandemic with his son Andrew has opened his eyes to the second major school: growth investing. Marks memo describes how now he has his son Andrew living with him, and Andrew is opening his eyes to the thinking of a growth investor.

Growth investing is about assigning a valuation to a company that may not yet have shown its value, but whose growth, as measured by one metric or another, has a potential to grow into cash flows of great value.

Recently, growth chasing has worked out very well. The one quote I’ll lift from Marks:

the performance of value investing lagged that of growth investing over the past decade-plus (and massively so in 2020)

It’s easy to understand why that might be. The speed at which the fast growing companies grow is almost incomprehensible. In 2002 the so-called facebook at Harvard was a physical book the college handed out with pictures of faces in it. In 2020, eighteen years later, one young person’s lifetime, $FB has two point five billion people using it every month. Facebook has swallowed up billions of dollars in advertising, helped wipe out at least two thousand local newspapers, and influences world events, from elections in the USA to ethno-religious violence in Burma.

Scary stuff, if you’re an innocent citizen. Groovy if you’re a shareholder of Facebook (I am not).

Or take Amazon:

For a sense of scale, it took Amazon more than 14 years—58 quarters after its May 1997 initial public offering—to make, cumulatively, as much profit as it produced in the latest quarter alone. Keep in mind that Amazon consistently lost money for its first several years as a public company.

(first article when I Google “when did Amazon finally make a profit?” ) From Wikipedia:

The company finally turned its first profit in the fourth quarter of 2001: $0.01 (i.e., 1¢ per share), on revenues of more than $1 billion.

A traditional value investor would not have been into Amazon in 2001.

The endgame for growth investing is you grow so big you’re the biggest animal in the pond and you have no competitors, only, in this pond example, small frogs to amuse you, and minnows to tickle your feet, and perhaps birds, and someone (local villagers? customers?) just keeps bringing you food because they have to. Or even want to? Or because of a curse? The example fails at this point but you get the idea.

Picking those winners can be hard. You need to choose what metrics of growth to focus on. The important metric may not be how much money you’re making. This seems to defy logic and economics and years of Wall Street lore, but that is how the market has reacted. The word is out that even if a company is not only not making money but is losing more and more money, that can in some cases be fine, that can still be fine, as long as they’re swallowing market share.

(This has created some funny wins for the consumer, like MoviePass).

So: value and growth. Marks’ memo is lucid well-expressed thinking on how his thinking is evolving about the blend of these two schools.

i just read the memo and agree, it is really good. love the idea that value investing just means buying something for less than it’s worth, even if that thing you’re buying is a fast growing company with a high current p/e multiple.

Now, there’s also technical investing, which seems to be people studying candlestick charts, and then trying to reverse-divine the algorithms that make automated trading decisions in Flash Boys style scenarios. I admire these folks, and there’s probably something to it, but it’s not for me.

There’s also momentum investing, where you chase where you think the herd is going, based on anything from complex systems of pattern recognition to just what people seem to be talking about and what’s in the headlines. I used to study this school, and it’s very fun.

What I’d like to propose is a new school.

Vibes Investing.

Vibes Investing we discussed on episode 7 of Stocks: Let’s Talk, with the legend Liz Hall.

We believe Vibes Investing has a bright future.

Is vibes investing even investing? Is growth investing investing? Most definitions of investing say something about “an expectation of achieving a profit,” or “a reasonable expectation.” What we’re talking about here may be something more like speculating. A different and perhaps equally noble pursuit.

The vibes speculator would not compete against the quants and the computers. The vibes speculator would look for signals the computer couldn’t see, invisible, unquantifiable signals. The vibes speculator would look for growth, but not according to any metric that might be spotted by a million growth investors. The vibes speculator would feel the growth.

I’ll have more to say on the topic of vibes speculating. I’ve considered launching a prestigious and expensive newsletter, The Vibes Speculator. Or perhaps a small book on the topic. I’m not sure if the book would be in the category “business” or “humor.”

If you control a budget at a well-funded company I’d consider giving a talk on vibes speculating for an extravagent fee.

If you have thoughts on vibes speculating, get in touch. It’s an exciting conversation.

(Disclaimer: none of what I say is investment advice of any kind. These are the musings of an enthusiastic amateur. If anything the sign that amateurs are talking about the stock market is a classic signal of a market top.)

The bank and the casino

Posted: January 18, 2021 Filed under: America Since 1945, business 2 Comments

The bank

In my hometown the bank building had a plaque on it, honoring Forbes McLeod, a policeman killed on Friday, Feb 2, 1934 in a gunfight with men robbing the bank. This bank robbery was considered of minor historical note as it was one of the first to involve machine guns.

The robbing of banks with guns has formed a theme of American movies possibly culminating in Heat (1995). What was the last good bank robbery movie? Before The Devil Knows You’re Dead (2007)? The Town (2010)? Has there been a good bank robbery movie in the last ten years? Who knows, maybe there will be another one soon.

The bank as “the place where the money is” has become less and less true. The bank buildings aren’t even impressive anymore. The bank as a physical place has become less significant.

If you have extra money, you have a good problem. What should you do with it*? “Put it in the bank” used to be a good answer. The money would be safe there. Even if the robbers took it, it would be covered. Right around the time Patrolman McLeod was killed, the Federal Deposit Insurance Corporation, FDIC, was formed.

Your money would be safe at the bank, and not only that, it would grow as it gained interest. Compounding interest is a powerful force, and this would be good. It was certainly better to put your money in the bank than to, say, take it to the casino.

However, many changes have happened since I was a kid being taken to the bank on a round of errands. These changes have happened very fast.

One change is that interest rates went down. And kept going down. This begins with the Federal Reserve Bank, and trickles down to your bank. The Federal Reserve is keeping interest rates down because it adds fuel (money) to the economy. Keeping money in the bank is a less good option as interest rates go down, so people don’t put money there, so more money flows around.

Another change that happened is that banks got deregulated**.

Restrictions on the opening of bank branches in different states that had been in place since the McFadden Act of 1927 were removed under the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994.

for instance. Conglomeration, mergers, big national and international banks could expand.

Deregulation also meant that banks got more and more freedom to take their deposit money and make all kinds of risky trades, hedges, and hedges of hedges with it. What the bank does now is bundle up money and take it over to the casino.

Sensibly enough, you may wonder if you should stop putting your extra money in the bank, and instead put it in the casino yourself.

The casino

Imagine a casino. Grand and intimidating. No one robs the casino, except Danny Ocean, and only when he has exactly the right ten for the crew, and that’s just in the movies. You don’t rob the casino because the casino is not screwing around. The casino might look funny on the outside, but that’s a trick. The casino is a machine to get as much money flowing through it as possible, and take some of the money.

The casino may look kind of appealing, especially when you keep seeing rich people walking out of it. But the casino is deadly serious. They wear suits in this casino. To even be allowed into the casino, you have to talk to a guy, maybe pay a fee.

Once you are inside, the casino is full of sharps. Some of the sharps are very, very rich. The players in the casino speak in sophisticated language that’s hard for you to understand. But if you can figure out the terms, you can place a bet on almost anything.

To place a bet in this casino is not free. The fee for a bet is about $8.95. Not only that, but many of the bets themselves are in significant amounts. There are bets you can make for a dollar or pennies (plus the fee). But some of the most popular bets are in minimum amounts of a hundred or even a thousand dollars.

These rules made this casino seem like something more serious and significant than like a casino casino, a Las Vegas casino. But just because this casino is on Wall Street doesn’t mean it’s not a casino.

Then, pretty rapidly, the rules of the casino change.

First, they get rid of the guy you need to talk to just to walk in. Now, you don’t need to talk to anybody. And there’s no cover. You don’t need to talk to anybody to place a bet. First they let you do that on your computer, and then when phones got good enough, they let you do it on your phone. There’s still a physical casino, but it’s sort of just for stock photos and background footage now. The casino is now totally online.

Next, the casino gets rid of the cost to place a bet. Now, there is no fee. Placing a bet is free.

Not only that, the casino starts marketing itself to young people, with colors and buttons. The online betting interface gets easier and easier. You can play in the casino as if it’s just another app on your phone, as easy to use as Instagram.

Just to eliminate one last hurdle the casino gets rid of the idea of minimum bet amounts. Now, you can do fractional bets, with however much money you have.

Very fast, the once grand and intimidating casino has changed, and now is more or less just an app where anybody place a bet on anything in any amount with no fee.

What happens to the casino, after these changes?

I don’t know, I’m trying to figure it out.

Are the old casino sharps inside happy? Or sad?

Maybe they’re happy at first – hey, lots of dumb money. But then they are overwhelmed. The dumb money changes the logic of the casino.

Do the sharps take their money to a new casino? Maybe even a secret casino? Do they band together and create alliances, even if this is technically against casino rules? Do they come up with new side games and bets?

I truly don’t know.

The friction that kept money from the casino and steered it to the bank has been eliminated. The safe and steady returns that lured money to the bank and away from the casino have been reduced. The bank and the casino are in business together now. Have the bank and the casino merged? They certainly flow together. Money is flowing from the bank to the casino, sure as sun follows moon.

It cannot be an accident that our outgoing president is a former casino operator. The president before him and the president before him and the president before him (who was raised in a casino town) were all surrounded, advised, and funded by leaders of the effort to merge the bank and the casino.

The incoming president was a senator from Delaware for almost forty years. Delaware is actually a real place: it has a population a little less than half that of San Bernardino County, 1/39th that of California. But legally what Delaware is is a jurisdiction for favorable rules for large-scale bank, casino, and bank-casino corporations.

Over half of publicly traded corporations listed in the New York Stock Exchange (including its owner, Intercontinental Exchange) and 60% of the Fortune 500 are incorporated (and therefore domiciled) in the state.

The bank and the casino may physically exist, somewhere, in a strip mall or a tall anonymous building, on Wall Street or in Delaware or in one of many downtown streets with big anonymous buildings, but it doesn’t matter. The bank and casino are all on your phone now.

What happens now?

I don’t know, I’m trying to figure it out.

My second-best speculation is to bet on the casino itself, because the federal government has revealed that one of its major goal if not its only true goal is keeping the bank-casino’s business growing.

My best speculation is that something totally unpredictable will happen. Rapidly growing complexity will have effects no one can predict, this is the lesson of both Jurassic Park and the Nicholas Nassem Taleb books. What happens when stuff like this starts happening?:

No one can predict, it cannot be modeled. After the fact there will be some sage identified who saw it all coming. If there are a million guesses, at least one will later appear kinda right. But it doesn’t really matter. No one can know with any confidence what will happen in such a system.

There could be a panic at the casino. Consider Larry McMurtry’s memory of a stampede he saw as a boy. He was helping to drive about one hundred cattle down an asphalt road:

Men, horses, and cattle were all drowsy, the herd just barely plodding along, until one cow happened to drag her hoof on the rough asphalt, making a loud rasping sound. In an instant that sleepy herd was in full flight, and our horses too. A single sound on a summer afternoon produced a short but violent stampede. The cattle and horses ran full-out for perhaps one hundred yards. It was the only stampede I was ever in, and a dragging hoof caused it.

A dragging hoof can cause a stampede, on a Texas farm-to-market road, or at the bank-casino. There doesn’t have to be a good reason.

Disclaimer: not investment advice, duh. I’m an amateur musing here.

* Jesus had a simple answer that solves this problem.

** in The Uprising: On Poetry and Finance, by Franco “Bifo” Berardi (semiotext(e), 2012) it’s claimed that the word deregulation was “first proposed by poet Arthur Rimbaud, and later reculced as a metaphor by neoliberal idealogues. Dérèglement des sens et des mots is the spiritual skyline of late modern poetry.”

John Malone

Posted: January 16, 2021 Filed under: America Since 1945, business Leave a comment

A man worth study.

At which point I discovered that there was a war about to explode on the scene for control of TelePrompTer between Cooke and Irving, and so I passed on the opportunity and Hub Schlafly ended up getting stuffed into that job for a while. Then I got an inquiry from Steve Ross at Warner and did I want to go do that? And unfortunately, the first thing I would have had to have done is have a difficult posture with the fellow that they had just bought a big company from and I didn’t really like that too much. Plus, the other issue there was New York headquarters. And while Steve said, “Well, you can live in Connecticut and have a limo” and all that kind of stuff, I didn’t think that was the life I was looking forward to. And then the third guy was Bob Magness, who was out here in Denver and Bob was just an intriguing kind of a guy and TCI was my kind of a company. They were so broke at the time that Bob used to say, “We’re so broke we’ve go to look up to see bottom. Lower than whale shit.” Very colorful expressions, but it was the opportunity I thought, in my mind, to get the family out of the New York metro and into clear and clean and beautiful Colorado, and so that’s the direction that… Oh, I took a 50% pay cut and agreed to buy a bunch of stock, which turned out to be underwater, very quickly, before I even got on the scene, but that brought me out to Denver. But they were guys that I had gotten to know over the prior couple of years – Sparkman and Bill Brazile and Carter Paige and Larry Romrell, Donne Fisher and I kind of liked them. I liked the attitude, it was a laid back kind of group.

from this conversation with Trgyve Myhren at The Cable Center

The first thing you learn is, once you make a guy rich, don’t expect them to work hard. Very unusual people do that.

How about this, from a 2012 lecture at the University of Denver:

I think the best example of vertical integration is, for instance, I get a phone call from Rupert Murdoch. He says, “CNN exists. I’ve got a company called News Corporation. I would love to have a cable television news channel in the United States. What do you think?” I say to him, “There’s probably room for another one, but you got to come down in terms of your political posture, a little bit to the right of center because CNN is going a little bit to the left of the center.” In the opinion of certainly people on the right [inaudible 00:19:32]. He says, “I think that’s great. Will you help me? i.e., will you invest with me?” and so we say, “Yes. What do you want us to do?” He said, “Why don’t you A, agreed to distribute our channel. B, I want you to go see if you can recruit Rush Limbaugh to be on my channel because I know him. C, how about 20% of this thing if it works?”

We launched Fox News Channel. We own 20% of it. We distribute it. He programs it. We take relatively little risk because we don’t put any money up. What we agreed to do was carry the channel, pay a fee per customer, an affiliate fee. It depends on him to do a good job of promoting it and creating. We end up owning 20% of what turns out to be a valuable asset. That’s the most no-brainer of the things you can do.

Or this:

There was a company called BlueMountain, traded for one and a half billion dollars, zero revenue. It was in the online greeting card business. You could go to BlueMountain and you could download a greeting card and you could send it off to your friends. It was free; had lots of traffic; never made the transition to economic viability. The Internet world was full of those bubble phenomenon, vaporware companies, we called them. They came and they went.

From a 2012 interview with Mark Robichaux at Multichannel News:

MCN: What about the threat of over-the-top players such as Netflix?

JM: I don’t know. I mean his (Netflix CEO Reed Hastings’) business model, of course, was to buy flat into the future and hope he grows into it. And if he doesn’t grow he’s got serious cash flow problems facing him. His stock has reflected debt, to some degree. I mean he’s got what, a couple-billion-dollar market cap? But that’s pretty low for 24 million subs.

I don’t see how Reed gets scale. That’s the curse for him. I mean he needs 40 million to 50 million households. I don’t see how he gets it if it’s split four ways.

MCN: Do you think Netflix, or any over-the-top player for that matter, can be a true competitor to cable?

JM: It all has to do with access to content. It really is about access to content.

The content that people care about, the content that will really move people, is pretty much controlled by big programmers like Disney, who are not about to shoot themselves in the foot. And so they are going to exploit it across all platforms in a very orderly and well thought through way. You know, right now cable has been a very effective monetization scheme for cable networks …

I was screaming at the Discovery [Communications] guys and the Starz guys about don’t shoot yourself in the foot with your Netflix thing. And ultimately, of course, Starz pulled back and Discovery was able to do a limited extension. Reed’s money is good, but I don’t know if he’s got a business model that really works for him.

Morgan Housel

Posted: January 9, 2021 Filed under: America Since 1945, business Leave a commentIn 1960 journalist Hugh Sidey attempted to gauge JFK’s economic credentials. “What do you remember about the Great Depression?” Sidey asked. Kennedy responded candidly:

I have no first-hand knowledge of the depression. My family had one of the great fortunes of the world and it was worth more than ever then. We had bigger houses, more servants, we traveled more. About the only thing that I saw directly was when my father hired some extra gardeners just to give them a job so they could eat. I really did not learn about the depression until I read about it at Harvard.

Morgan Housel, who writes this semi-regular column for The Collaborative Fund, has a great gift for historical anecdotes. How about this one:

The Battle of Stalingrad was the largest battle in history. With it came equally superlative stories of how people dealt with risk.

One came in late 1942, when a German tank unit sat in reserve on grasslands outside the city. When tanks were desperately needed on the front lines, something happened that surprised everyone: Almost none of the them worked.

Out of 104 tanks in the unit, fewer than 20 were operable. Engineers quickly found the issue, which, if I didn’t read this in a reputable history book, would defy belief. Historian William Craig writes: “During the weeks of inactivity behind the front lines, field mice had nested inside the vehicles and eaten away insulation covering the electrical systems.”

The Germans had the most sophisticated equipment in the world. Yet there they were, defeated by mice.

You can imagine their disbelief. This almost certainly never crossed their minds. What kind of tank designer thinks about mouse protection? Nobody planned this, nobody expected it.

But these things happen all the time.

“These things happen all the time” reminds me of the opening of the movie Magnolia.

Hold your breath

Posted: January 7, 2021 Filed under: America, America Since 1945 Leave a commentSenator Mitt Romney of Utah, the lone Republican who voted to convict Trump in last year’s impeachment trial, pointed out that there’s little time for either an impeachment or what likely would be a drawn out battle over the Constitution’s 25th Amendment, which provides for the removal of a president.

“I think we have to hold our breath,” he told reporters.

Is that gonna be the plan, in this country? We’re a lucky country, but nobody’s lucky forever. (it’s like this bit!)

(source for that bit: Steven T. Dennis and Billy House for Bloomberg)

Top 8 of 2020

Posted: December 27, 2020 Filed under: America Since 1945 Leave a comment

We’re pleased with our small, distinguished, growing audience. These were our most popular posts of the year.

about how JFK spent the night before the 1960 Wisconsin primary. Somebody wrote in to correct me that the movie in question was more like “sexploitation” than porn, but “porno” is the word Bradley used.

grateful this year that we got a chance to see Chaco Canyon, walking the site only increased the fascination

One Two Three Four: The Beatles In Time by Craig Brown.

The book has been released here as 150 Glimpses of the Beatles. What’s great about Craig Brown is that he goes to the sources, the primary sources, and tells you not just the details of the incident, but the historiography, the story of the story.

always a popular top.

another inspiration. Got a beautiful note from Vickers’ daughter which was really touching, glad we could add to the information available about this remarkable man.

The Wanderer’s Hávámal by Jackson Crawford

Glad to be introduced to this stunning work in a readable translation. Why not let the Norse gods advise you on how to conduct yourself when you travel?

This is just an image we found somewhere else, it’s illuminating.

Couple others that found their way: Marilyn Monroe gossip, How to Read A Racing Form, and Conversations With.

We had a nice guest post this year, Founding Documents by Billy Ouska. We’d love to have more of those in 2021.

Hope you’re all keeping well and safe.

Empire States of Mind

Posted: December 15, 2020 Filed under: America Since 1945, economist, New York Leave a comment

Peter Thiel cites the fact that the Empire State Building was built in 15 months as a sign that maybe our society has stagnated. Can we build things any more? Why not?

I’ve wondered if part of the answer was the political power of Al Smith, who was appointed head of Empire State Inc, and various other elements of the former Tammany/Democratic machine that controlled New York City at the time. An argument for the efficiency of political machines?

But what if the answer was: fairness?

The Empire State Building was constructed in just 13* months, and that included the dismantling of the Waldorf-Astoria hotel that sat on the site. Paul Starrett, the builder, treated his workers rather well by the standards of the time, paying much attention to safety and paying employees on days when it was too windy to work. Daily wages were more than double the usual rate and hot meals were provided on site.

The concept is known as “efficiency wages”. Companies that compensate workers well and treat them fairly can attract better, more motivated staff. Unlike most construction projects, the Empire State Building had low staff turnover, and workers suggested productivity improvements such as building a miniature railway line to bring bricks to the site.

That’s Bartleby in the Dec 12, 2020 Economist, reviewing a book called The Art of Fairness, by David Bodanis. Starrett was not “naively generous,” the article also notes. He checked worker attendance four times a day.

I’d kind of resolved to stop reading these books that are just collections of neat anecdotes under some big umbrella, but maybe I’ll make an exception here. Another example cited: Danny Boyle used thousands of volunteers for the 2012 London Olympic Ceremonies, but he also had to keep details of the show secret:

The conventional approach would have been to make the volunteers sign a non-disclosure agreement. Instead, he asked them to keep the surprise – and trusted them to do so. They did, thanks to the grown up way he treated them.

Also in this week’s Economist, Buttonwood reports on a study in India:

The study’s main finding is that retail investors who were randomly allocated shares in successful IPOS view their good fortune as evidence of skill.

* note the revision to Thiel’s figure

Mile Marker Zero: The Moveable Feast of Key West by William McKeen

Posted: September 24, 2020 Filed under: America Since 1945, Florida, Hemingway, writing Leave a comment

This is a book about a scene, and the scene was Key West in the late ’60s-’70s, centered on Thomas McGuane, Jim Harrison, Hunter Thompson, Jimmy Buffett, and some lesser known but memorable characters. I tried to think of other books about scenes, and came up with Easy Riders, Raging Bulls by Peter Biskind, and maybe Astral Weeks: A Secret History of 1968 by Ryan H. Walsh, about Van Morrison’s Boston. Then of course there’s Hemingway’s A Moveable Feast, referenced here in the subtitle, a mean-spirited but often beautiful book about 1920s Paris.

I was drawn to this book after I heard Walter Kirn talking about it on Bret Easton Ellis podcast (McGuane is Kirn’s ex-father-in-law, which must be one of life’s more interesting relationships). I’ve been drawn lately to books about the actual practicalities of the writing life. How do other writers do it? How do they organize their day? What time do they get to work? What do they eat and drink? How do they avoid distraction?

From this book we learn that Jim Harrison worked until 5pm, not 4:59 but 5pm, after which he cut loose. McGuane was more disciplined, even hermitish for a time (while still getting plenty of fishing done) but eventually temptation took over, he started partying with the boys, eventually was given the chance to direct the movie from his novel 92 In The Shade. That’s when things got really crazy. The movie was not a big success.

“The Sixties” (the craziest excesses bled well into the ’70s) musta really been something.

On page one of this book I felt there was an error:

That’s not the line. The line (from the Poetry Foundation) is:

The best laid schemes o’ Mice an’ MenGang aft agley,

Part of what these writers found special about Key West, beyond the Hemingway and Tennessee Williams legends, was it just wasn’t a regular, straight and narrow place. Being a writer is a queer job, someone’s liable to wonder what it is you do all day. In Key West, that wasn’t a problem.

Key West was so irregular and libertine that you could get away with the apparent layaboutism of the writer’s life.

Some years ago I was writing a TV pilot I’d pitched called Florida Courthouse. I went down to Florida to do some research, and people kept telling me about Key West, making it sound like Florida’s Florida. Down I went on that fantastic drive where you feel like you’re flying, over Pigeon Key, surely one of the cooler drives in the USA if not the world.

The town I found at the end of the road was truly different. Louche, kind of disgusting, and there was an element of tourists chasing a Buffett fantasy. Some of the people I encountered seemed like untrustworthy semi-pirates, and some put themselves way out to help a stranger. You’re literally and figuratively way out there, halfway to Havana. The old houses, the chickens wandering, the cemetery, the heat and the shore and the breeze and the old fort and the general sense of license and liberty has an intoxicating quality. There was a slight element of forced fun, and trying to capture some spirit that may have existed mostly in legend. McKeen captures that aspect in his book:

Like McGuane, I found the mornings in Key West to be the best attraction. Quiet, promising, unbothered, potentially productive. Then in the afternoon you could go out and see what trouble was to be found. Somebody introduced me to a former sheriff of Key West, who helped me understand his philosophy of law enforcement: “look, you can’t put that much law on people if it’s not in their hearts.”

I enjoyed my time there in this salty beachside min-New Orleans and hope to return some day, although I don’t really think I’m a Key West person in my heart. I went looking for photos from that trip, and one I found was of the Audubon House.

After finishing this book I was recounting some of the stories to my wife and we put on Jimmy Buffett radio, and that led of course to drinking a bunch of margaritas and I woke up hungover.

I rate this book: four and a half margaritas.

The illusion of choice

Posted: September 19, 2020 Filed under: America Since 1945, business Leave a comment

Cool graphic, from “Monopolies are Distorting the Stock Market” by Kai Wu of Sparkline Capital

{kind=link}

{kind=link}

{kind=link}

{kind=link}