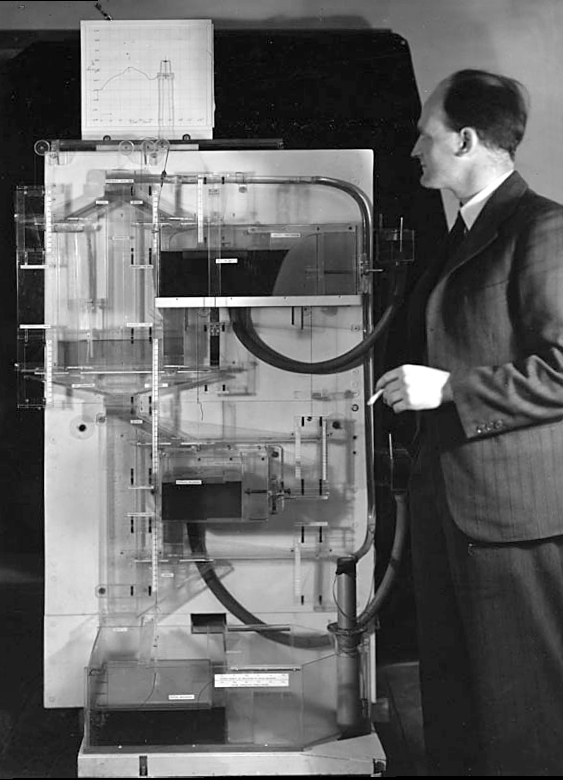

MONIAC

Posted: January 27, 2026 Filed under: money Leave a commentThere’s a visual metaphor for the process [of economists getting lost in models and trying to apply principles to reality] in the form of an amazing device called the Phillips machine, the creation of a remarkable New Zealander called Bill Phillips. After a roundabout route to the world of economics via a spell in a Japanese prisoner-of-war camp, Phillips set up a workshop in a south London garage. There, using recycled Lancaster bomber parts, he botched together a machine that used the flow of water to demonstrate the functioning of the entire British economy. There was a point at which these machines, known as MONIACs—Monetary National Income Analogue Computers—were all the rage: there are about twelve of them (no one knows exactly how many were built) in places as diverse as the central bank of Guatemala, the University of Melbourne, Erasmus University in Rotterdam, and Cambridge, England, which has the only one that works. The Phillips machines/MONIACs were fine-tuned to simulate different economic conditions: the New Zealand one, for instance, was set up to match the specific dynamics of the New Zealand economy.

That’s from How To Speak Money by John Lanchester.

(source)

Lanchester continues:

Phillips was a serious man, who partly on the basis of his machine became a professor of economics at LSE, and he had a serious specific concern in creating the MONIAC, to do with stabilizing demand inside the economy. And yet, it’s hard not to see his machine as a comic allegory of what’s called wrong in the model-making side of economics. It’s inherently comic in the way that a Roz Chast cartoon is inherently comic. The idea that this thing can simulate something as big and complicated as an entire economy—really? And yet, that’s what economic models set out to do all the time. The Federal Reserve and US Treasury are to this day reliant on models of exactly this sort; their models are built out of mathematics rather than out of bomber parts and water, but the underlying principles are the same. Credit flows and monetary supply, inflation rates and external shocks and trade imbalances and fluctuations in demand and tax changes are all modeled in an exactly analogous way.

(source, the cigarette is a great touch)

Phillips:

During this period he learned Chinese from other prisoners, repaired and miniaturised a secret radio, and fashioned a secret water boiler for tea which he hooked into the camp lighting system.[4] Sir Edward ‘Weary’ Dunlop explained that Phillips’ radio maintained camp morale, and that if discovered, Phillips would have faced torture or even death.[7]

Coins

Posted: November 7, 2022 Filed under: business, money Leave a comment

say what you will about Queen Elizabeth she looks good on a coin. I wonder if some of the turbulence in UK markets of late have to do with the fact that Steady Grandma will no longer be on the money, now it is Weird Son.

French coin picked up most likely in Tahiti

The Euro’s kind of ominous, no?

The guinea and the ETH

Posted: December 23, 2021 Filed under: money Leave a commentThe guinea was an English unit of currency, minted as a coin between 1663-1814. Today you won’t find guinea coins or notes, but a guinea still exists as an idea, at least among a certain class.

A guinea is 21 shillings, versus a pound, 20 shillings. Some kinds of high-status bills were reckoned in guineas: solicitor or barrister fees, for example, bespoke tailoring, or gentlemen’s wagers. There is a famous horse race, the 2000 Guineas.

Bids are still made in guineas for the sale of racehorses at auction, at which the purchaser will pay the guinea-equivalent amount but the seller will receive only that number of pounds. The difference (5p in each guinea) is traditionally the auctioneer’s commission (which thus, effectively, amounts to 5% on top of the sales price free from commission).

The guinea as idea like much distinct and unique in England is mostly vanished now, I’ve never paid a debt in guineas or heard of anyone doing so, it’s from the past. But I thought of the idea of the guinea while trying to understand Ethereum, ETH.

As far as I can tell, ETH is the currency of the NFT market. NFTs, which you’ve probably heard are “non-fungible tokens” or a digital art form, the most desired examples of which are trading at very high prices, at least in ETH, which translates to the dollar at a fluctuating price, currently somewhere around $1=.00024 ETH, or 1 ETH = $4,113.23. I am told that ETH is also somehow “useful,” “you could build a whole economy on it,” it’s a basis for trustless transactions, I don’t understand that. I keep trying to but it involves watching YouTubes of people who seem like they took too many nootropics.

But I am interested in a prestige currency for a niche art market.

Bretton Woods Is No Mystery and The Nixon Shock

Posted: March 7, 2021 Filed under: America Since 1945, business, money, New England Leave a commentBreaking the Breton Woods agreements, the American president said that the dollar would have no reference to reality, and that its value would henceforth be decided by an act of language, not by correspondence to a standard or to an economic referent.

That’s from The Uprising: On Poetry and Finance, by Italian communist Franco “Bifo” Berardi, published by semiotext(e). Full of interesting ideas.

Everywhere I turn these days, from the new Adam Curtis documentary to the Bitcoin-heads on Twitter, I hear about Sunday, August 15, 1971. On that evening, Richard Nixon, conferring with his advisors in a weird weekend at Camp David, went on TV and announced he was taking the US dollar off the gold standard. Nixon ended the “Bretton Woods system.”

Always had an interest in the Bretton Woods system. Worked out at the Mount Washington Hotel in Bretton Woods*, New Hampshire. My dad and I went cross-country skiing up there.

The hotel shut up for winter had a spooky, imposing quality.

President Franklin Roosevelt proposed the conference site, the Mount Washington Hotel, as a ploy (successful, as it turned out) to win over a likely opponent of the pact, New Hampshire senator Charles Tobey.

That’s from Michael A. Martorelli’s review of Benn Steil’s book about the conference, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order.

The conference happened in July 1944. The Allied forces were stalled in the bocage of Normandy. But leadership was planning for the postwar order. John Maynard Keynes, who’d studied the disaster of the last postwar peace, was trying to avoid the same mistakes while attempting to save the dignity of the UK. Keynes suggested the world switch to a global currency called Bancor. The US, represented by Harry Dexter White, dominant, had the strong position. The US proposed to leave the US dollar, pegged to gold, as the world’s reserve currency.

Deeply indebted to the United States after the long, costly ordeal of World War II, the United Kingdom inevitably lost the battle. To secure one key victory, however, White had to resort to stealth. In the waning hours of the conference, he and his assistants replaced the phrase “gold” with “gold and US dollars” in the agreement, thereby enshrining the US currency as the international medium of exchange. Keynes confessed that he did not read the final version of the document he signed.

You think there aren’t thrills in a book about a 1944 economic conference whose results have been overturned? Wrong:

In one noteworthy coup, [Steil] disproves Keynes biographer Robert Skidelsky’s claim that Keynes was assigned Room 129 in the Mount Washington Hotel.

The summit does sound exciting. The Soviets brought a bunch of female “typists” to seduce everyone.

One committee of delegates took a 15-minute recess in the bar each night at 1:30 to watch the “titillating gyrations of Conchita the Peruvian Bombshell.” Afterward, reinvigorated, they would negotiate for another hour or so. The long arguments left White increasingly short-tempered on less than five hours of sleep a night. Keynes, already weakened by the heart disease that would kill him within two years, was soon holding court from his bed, tended (and guarded) by Lydia, his eccentric Russian ballerina wife. At one point, a rumor spread that he was near death; when he then appeared at dinner, the delegates spontaneously stood and sang “For He’s a Jolly Good Fellow.”

from a different review of a different book about the conference:

I’ve taken a look at both Steil and Conway’s books. The Summit by Conway is more fun and easy to read, and focuses on the wild details – what he calls the “noises off” stuff – from the conference. The drunken songs, the parody newspaper about the “International Ballyhoo Fun,” the pleasure delegates from wartorn countries took in plates of “chicken Maryland” and bowls of ice cream, the South Africans playing golf once it was clear gold wouldn’t be replaced by silver, the results of the Soviet vs USA volleyball game (USSR won), that’s in Conway.

The details of the conference are interesting, but the outcome was inevitable. The US was the last power standing as World War II ended. The UK was in our debt (literally). What we ended up with was the system we devised: the dollar as default world currency.

The true significance of the conference was noted by Keynes in a speech at the farewell dinner:

We have shown that a concourse of 44 nations are actually able to work together at a constructive task in amity and unbroken concord. Few believed it possible. If we can continue in a larger task as we have begun in this limited task, there is hope for the world.

If you read one review of one book about the conference, read James Grant’s review of Steil in the Wall Street J (behind a paywall, they’re no fools about money at the WSJ):

Gold figures largely in these pages. The ancient metal was deeply rooted in the psyche of Keynes’s contemporaries, including that of Lt. Col. Sir Thomas Moore, a British Conservative member of Parliament. In parliamentary debate, Sir Thomas said that he had “the impression, not being an economist, that currency had to be tied to or based on something; whether it was gold, or marbles, or shrimps, did not seem to matter very much, except that as marbles are easy to make, and shrimps are easy to catch, gold for many reasons possessed a more stable quality.” For the soundest doctrine expressed in the fewest words, Sir Thomas was hard to beat.

Grant, if you can’t read it, isn’t too boosterish on the Bretton Woods system:

Rare among nations, America pays its overseas debts in money that it alone may lawfully print. Naturally, being human, we Americans have printed to excess. Not since 1975 has the United States exported more goods and services than it has imported. There is no institutional check to square up accounts. We buy Chinese merchandise with dollars. The Chinese, in turn, invest those dollars in U.S. government securities (the better to suppress the value of the Chinese currency). It’s as if the money never left the 50 states. In possession of the “reserve currency” franchise—White’s dream fulfilled—America has become the world’s leading debtor nation. At Bretton Woods, it was the world’s top creditor.

Mentioned the Nixon Shock to a bud who works at a hedge fund, and he put me on to WTF Happened in 1971, which takes a darker view. Love the idea that this is the moment everything went wrong and reality broke, but I’m not convinced. What about the Triffin dilemma? Was Nixon changing reality, or acknowledging it?

Consider how things worked before Bretton Woods. Both Conway and Stiel note that FDR would dictate the dollar price of gold from bed in the morning, once raising the price by twenty-one cents because that was a lucky number. This was more “real”?

A crazy element of the conference is that the leader of the US delegation, Harry Dexter White, was communicating with the Soviets. To what extent he was a traitor, a spy, vs kind of backchannel with our wartime ally is unclear. But declassified transcripts make clear he was a Soviet asset known at “Jurist” or “Richard.” That’s if you trust our own NSA. Who knows?

White testified in front of HUAC that he was not a Communist, then had a heart attack. He went to his home in New Hampshire and died four days later.

Is it possible White sabotaged the US team in the Bretton Woods volleyball game? To provide a propaganda win for his Soviet masters? The Russians got a lot of concessions at Bretton Woods to induce them to sign on to the agreements. But I don’t see in Steil or Conway any case that White’s possible connection helped them. Conway is a skeptic on the spy stuff, suggesting that yes, it looks fishy, but it’s impossible to prove White “betrayed his country.”

One person who would’ve known White had been a spy? President Richard Nixon.

Following Alger Hiss’s perjury conviction in 1950, Representative Richard M. Nixon revealed a handwritten memo of White’s given to him by Chambers, apparently showing that White had passed classified information for transmission to the Soviets. Yet his guilt would only be firmly established after publication of Soviet intelligence cables in the late 1990s.

The IMF and World Bank linger as Bretton Woods legacies. Conway in his epilogue notes how even after the demise of the Bretton Woods system, the IMF still imposes the “Washington Consensus” on the developing world in return for loans. Maybe someone should activate the Coconut Clause:

Conway also notes that after the demise of the system, US and British banks became more profitable.

In the United States, by the turn of the millennium banks now accounted for around 8 per cent of the country’s total economic output – more than double their zie when the Bretton Woods system ended… Until 1970, an investor in a UK bank could expect to make about 7 per cent a year on his investment. After 1970, the return on equity roughly trebled to 20 per cent, a figure maintained without a break until the financial crisis of 2008.

There is no single, simple explanation for this astonishing rise of the financial sector; however, there is no doubt that one important element is the sudden change in the international monetary architecture following the collapse of Bretton Woods. Almost immediately after the demise of Keynes and White’s system in the early 1970s, every single measure of the size, profitability, and leverage of the banking industry has begun to increase at unprecedented rates.

The big banks in the USA tried to stop Bretton Woods at the time,

After the Bretton Woods conference, the countries involved had to sell it to a confused public. One method the USA used was a pamphlet called Bretton Woods Is No Mystery, illustrated by the New Yorker cartoonist Syd Hoff. I’m on the trail of a copy, I can only find a few images online.

Heartbreaking to hear the names bandied about for the world currency, and think what might’ve been. From Conway:

among the suggestions were Fint, Proudof, Unibanks, Bit, Pondol, and Keynes’ favorite, Orb. Months later, Keynes sent round a note to his Treasury colleagues asking: “Do you think it is any use to try unicorn on Harry?”

What do you guys think will be the world’s reserve currency in 2031? Dogecoin?

*an archaic name for what’s now part of Carroll, New Hampshire.

How much would you pay for this painting?

Posted: June 27, 2019 Filed under: art history, money 1 Comment

Basquiat’s “Pink Elephant with Fire Engine,” depicting cartoonish images on yolk-colored background, hammered at 2.2 million pounds, falling short of the low estimate of 3 million pounds.

The Gambler (2014)

Posted: September 12, 2018 Filed under: business, film, money, movies, screenwriting, shakespeare, writing 1 Comment

Saw this clip on some retweet of this fellow’s Twitter.

I was struck by

- the bluntness and concision of the advice

- the fact that the advice contains a very specific investment strategy down to what funds you should be in (80% VTSAX, 20% VBTLX)

- the compelling performance of an actor I’d never seen opposite Wahlberg (although I’d say it drops off at “that’s your base, get me?”)

It appeared this was from the 2014 film The Gambler

The film is interesting. Mark Wahlberg plays a compulsive gambler and English professor. There are some extended scenes of Wahlberg lecturing his college undergrads on Shakespeare, Camus, and his own self-absorbed theories of literature, failure, and life. The character is obnoxious, self-pitying, logorrheic and somewhat unlikeable as a hero. Nevertheless his most attractive student falls in love with him. William Monahan, who won an Oscar for The Departed, wrote the screenplay. The film itself is a remake of 1974 movie directed by James Toback, in which James Caan plays the Mark Wahlberg role.

Here’s the interesting thing. Watching the 2016 version, I realized the speech I’d seen on Twitter that first caught my attention is different. The actor’s different — in the movie I watched it’s John Goodman.

What happened here? Had they recast the actor or something? The twitterer who put it up is from South Africa, did they release a different version of the movie there?

Did some investigating and found the version I saw was made by this guy, JL Collins, a financial blogger.

Here’s a roundup of his nine basic points for financial independence.

He did a pretty good job as an actor I think! I believe the scene in the movie would be strengthened from the specificity of his advice. And the line about every stiff from the factory stiff to the CEO is working to make you richer is cool, maybe an improvement on the script as filmed. I’ll have to get this guy’s book.

It would make a good commercial for Vanguard.

VTSAX vs S&P 500:

Readers, what does the one to one comparison of JL Collins and John Goodman teach us about acting?

Why Ben Graham wouldn’t hire Warren Buffett

Posted: August 18, 2018 Filed under: business, money Leave a comment

If you read anything at all about investing, pretty soon you will hear about Ben Graham, father of value investing and teacher of Warren Buffett.

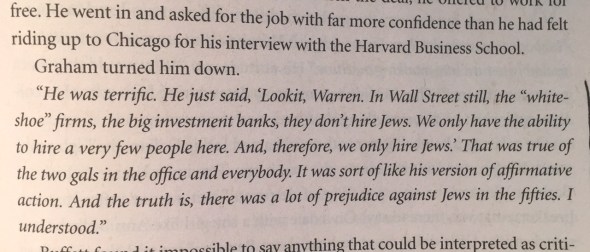

Young Warren Buffett got an A+ in Graham’s class at Columbia Business School, and would later work for Graham. But when he first asked Graham for a job, in fact offered to work for free, Graham (born Grossbaum) wouldn’t hire Buffett. Why? The story in Buffett’s own words:

I’d never heard that one before. It’s in:

Later, Graham would hire Buffett, and he got to wear the signature gray jacket that absorbed ink stains from writing down rows of figures.

I found this book more compelling than I expected. By the time Buffett was in tenth grade he owned a forty acre farm in Nebraska he’d bought with paper route money. You can read an interesting interview with author Alice Schroeder here:

Miguel: Give us advice to becoming better communicators.

Alice: Well…this is not anything profound. But you see that he uses very short parables, stories, and analogies. He chooses key words that resonate with people —that will stick in their heads, like Aesop’s fables, and fairytale imagery. He’s good at conjuring up pictures in people’s minds that trigger archetypal thinking. It enables him to very quickly make a point … without having to expend a lot of verbiage.

He’s also conscientious about weaving humor into his material. He’s naturally witty, but he’s aware that humor is enjoyable and disarming if you’re trying to teach something.

And here’s Michael Lewis reviewing the book.

Ben Graham by the way ultimately got kinda bored of investing and retired to California where he had a relationship with his late son’s girlfriend.

A great detail:

Perspective on Bitcoin

Posted: June 12, 2018 Filed under: business, money Leave a comment

Eric Guinthier put this on Wikipedia.

was thinking about this as I tried to remember some login or another: there’s no way in Hell all these numbnutses are gonna remember all their blockchain passwords and cryptokeys and what have you. The panicked runs on cryptocurrencies are gonna be crazy.

Maybe I should start a dump or an ewaste junkyard, eight bucks to throw away your old hard drive, and wait around for some panicked nerd to come screaming that he threw away seventeen million dollars in unharvested Ripple or whatnot.

that picture above is of Yap stone money. When someone tries to explain the history of money, sooner or later they’ll mention the stone money of Yap, usually avoiding an opinion on whether or not using enormous stone wheels as money is completely ridiculous.

Because these stones are too large to move, buying an item with one simply involves agreeing that the ownership has changed. As long as the transaction is recorded in the oral history, it will now be owned by the person it is passed on to and no physical movement of the stone is required.[citation needed]

(lol at citation needed. God bless Wikipedia. You try and write up Yap money in your spare time and someone comes along demanding footnotes).

Beades on Wikipedia took this picture of a rai stone at the Bank of Canada Currency Museum in Ottawa. How much do you think they paid for it?

Highlights from Warren Buffett’s 2018 letter

Posted: February 24, 2018 Filed under: business, money Leave a comment

Another good one drops from Warren Buffett and the Berkshire Hathaway team.

In America, equity investors have the wind at their back.

We’ve learned a great deal here at Helytimes from studying Buffett’s writings. Here’s a writeup on the 2017 letter and on the 2016 letter and from a book of quotes from his letter.

A highlight from this year, worth noting:

The $65 billion gain is nonetheless real – rest assured of that. But only $36 billion came from Berkshire’s operations. The remaining $29 billion was delivered to us in December when Congress rewrote the U.S. Tax Code.

Did not know about the stake in Pilot Flying J:

How did Warren Buffett get so rich? Some answers he will tell you.

- By gathering money, eventually including the enormous pools of money (“float”) collected by insurance companies like GEICO

- Using the money to buy shares of businesses with a durable competitive advantage (here’s a critical take on what that can mean)

- Never selling anything so that he’s never taxed on the gains and the results compound and compound.

For the last 53 years, the company has built value by reinvesting its earnings and letting compound interest work its magic.

(Also he just seems to have an intuitive and unusually focused mind for business:

As a teenager, he took odd jobs, from washing cars to delivering newspapers, using his savings to purchase several pinball machines that he placed in local businesses.

Also he did some arbitrage things I don’t understand.)

In this letter, he discusses the result of a bet he made that an unmanaged index fund would beat selected hedge funds over a ten year period:

I made the bet for two reasons: (1) to leverage my outlay of $318,250 into a disproportionately larger sum that – if things turned out as I expected – would be distributed in early 2018 to Girls Inc. of Omaha; and (2) to publicize my conviction that my pick – a virtually cost-free investment in an unmanaged S&P 500 index fund – would, over time, deliver better results than those achieved by most investment professionals, however well-regarded and incentivized those “helpers” may be.

Addressing this question is of enormous importance. American investors pay staggering sums annually to advisors, often incurring several layers of consequential costs. In the aggregate, do these investors get their money’s worth? Indeed, again in the aggregate, do investors get anything for their outlays?

More:

A final lesson from our bet: Stick with big, “easy” decisions and eschew activity. During the ten-year bet, the 200-plus hedge-fund managers that were involved almost certainly made tens of thousands of buy and sell decisions. Most of those managers undoubtedly thought hard about their decisions, each of which they believed would prove advantageous. In the process of investing, they studied 10-Ks, interviewed managements, read trade journals and conferred with Wall Street analysts. 13 Protégé and I, meanwhile, leaning neither on research, insights nor brilliance, made only one investment decision during the ten years. We simply decided to sell our bond investment at a price of more than 100 times earnings (95.7 sale price/.88 yield), those being “earnings” that could not increase during the ensuing five years. We made the sale in order to move our money into a single security – Berkshire – that, in turn, owned a diversified group of solid businesses. Fueled by retained earnings, Berkshire’s growth in value was unlikely to be less than 8% annually, even if we were to experience a so-so economy.

Fewer good jokes this year, in our opinion, but also fewer dire warnings.

Update on Norway’s sovereign wealth fund

Posted: September 27, 2017 Filed under: money Leave a comment

from Wiki user Michael Haferkamp

It’s now at one trillion dollars.

Previous coverage on Norway’s sovereign wealth fund.

What do these buildings have in common?

Posted: October 10, 2016 Filed under: California, money, New York, San Francisco Leave a commentOne Beacon Street, Boston

![]()

425 Market Street, San Francisco:

11 Times Square, New York:

Along with a lot of other buildings in Boston, New York, San Francisco, Paris, London and elsewhere, they’re all 47% or so owned by the Norwegian people, in the form of their nation’s sovereign wealth fund.

They own a lot of other stuff, too. $21 mill worth of Buffalo Wild Wings, for instance.

And 1.5% of Whole Foods:

In a tiny way, every Norwegian helps Marc Maron, because they own about a million bucks worth of Stamps.com.

{kind=link}

{kind=link}

{kind=link}

{kind=link}