Publicly traded American restaurant groups

Posted: March 22, 2024 Filed under: business, food 1 Comment

Bloomin Brands (ticker symbol: BLMN) owns Outback Steakhouse and Fleming’s. 50 new Outback Steakhouses opened in Brazil since 2021.

There are 3,427 Chipotles (CMG) in the United States, with 97,660 employees. Here’s Slate recently on Chipotle’s dominance:

But despite that backlash, the fact remains that for a lot of Americans, from San Diego to New Haven and everywhere in between, Chipotle has become effectively synonymous with good Mexican eating. When the Wall Street Journal interviewed Mary Hawkins, the mayor of Madison, Mississippi—one of the tiny population centers Chipotle has in its sights—she said the town had recently polled its citizenry about the brands it would most like to see take up residence on its streets. Chipotle, perhaps unsurprisingly, came in first, and Arellano does not see that trend slowing down.

“It’s like Galactus from Marvel Comics. It’s eating up burrito cultures from across the country,” he said. “Chipotle taught an entire generation of Americans to eat a very specific style of burrito. If they want a burrito, they’re going to want the one they grew up with and neglect the other styles.”

McDonald’s (MCD) of course is the king, with 42,000 stores. Here’s Ian Borden, McDonald’s CFO, being interviewed at a UBS conference:

Dennis Geiger

That’s great. Want to go over to core menu. And you just talked about some of the opportunities at chicken I think in particular. As we think about beef, chicken and coffee and some of the biggest opportunities to kind of further your advantages on core menu anything else to kind of highlight there across those key equities?

Ian Borden

Yes. Sure. Well look I talked about core is critically important. 65% of our global system-wide sales, $17 billion brands across that core categories and I think a few headlines under each of those three. Beef obviously we’re by far the largest player in beef globally. We’ve gained share since 2019 pretty consistently across our markets. I think a couple of the key things from an opportunity standpoint in beef. Best Burger which is just a series of what I’ll call small changes in how we cook and prepare our core beef products that’s been out to about 70 markets. It’s going to be in the rest of the system by end of 2026. It’s driving significant improvements in taste and quality. Taste and quality are the two biggest drivers of consumer visits to our restaurants. So that’s impactful.

The second thing on beef that I think is worth highlighting is the opportunity we see around large burger. And it’s a good example of how I think we are more precisely understanding consumer need and then getting after that consumer need and I’ll call it a one-way approach. So we’ve tried to get after this opportunity for a number of years because we thought the opportunity was about premium burger which was wrong. And we — so we didn’t — we weren’t successful. We now understand what the opportunity is for a large more satiating-type burger. That opportunity is significant. It’s consistent across many of our large markets.

And we have innovated a couple of products that we’re in the process of piloting. We’re going to pilot those products in two or three what we call market zeros. We’re then going to — if those products work we’re then going to scale one solution to that opportunity globally where in the past you would have seen us probably try and get after that opportunity in 20 different markets in 20 different ways and then you don’t have the ability to build a global equity that you can drive at scale. So that’s a little bit about beef.

McDonald’s is essentially a real estate company with a restaurant system they can affix and then turn over to franchisees.

The Darden Group (DRI) owns: Ruth’s Chris Steak House, Eddie V’s and The Capital Grille, Olive Garden Italian Restaurant, LongHorn Steakhouse, Bahama Breeze, Seasons 52, Yard House and Cheddar’s Scratch Kitchen. Until July 28, 2014, Darden also owned Red Lobster. Darden has more than 1,800 restaurant locations and more than 175,000 employees, making it the world’s largest full-service restaurant company. (says Wikipedia). There are 77 Ruth’s Chris and 562 Longhorn Steakhouses.

Brinker (EAT) has Chili’s and Maggiano’s Italian Grill. They’re having a killer year, surprising to me to learn, as the local Maggiano’s is closed and troughs of Italian slop don’t seem in fashion. But my heart still warms at the thought of Chili’s. Norman Brinker was a pioneer of the casual dining space.

Dine (DIN) owns IHOP (1,787 restaurants), Applebee’s (1,654) and Fuzzy’s Taco Shop (137 branches). The local IHOP near me is closing. A few years ago I tried an Applebee’s and was dissatisfied with the experience. I’ve never even seen a Fuzzy’s. As for pancakes, feels like they peaked as a food in like 1880?

Domino’s has 20,197 franchises. Their stock (DPZ) over the last twenty years returned investors something like 2,600% (vs 239% for the S&P 500). The key is the easy to use app.

Restaurant Brands International (QSR) has Burger King, Tim Horton’s, Popeyes, and Firehouse Subs, for a total fo 30,375 franchises. Noted investor and Harvard administration gadfly Bill Ackman has a big position in QSR, as well as Chipotle. In his recent Lex Friedman podcast he noted that some of his biggest wins have been in restaurants.

Shake Shack (SHAK) has expanded very fast, they now have 440 stores. I remember going to the very first branch in the summer of 2009, before starting my new job on 30 Rock. Who was in line behind me but Scott Adsit?!

Texas Roadhouse (TXRH) is booming, returning 738% for investors since founding. The story of founder W. Kent Taylor is worthy of its own post, when I have the time. I listened to a couple podcasts, one with Jerry Morgan, current CEO and one with VP of communications Travis Doster, and they project a “fun with purpose” coherent and vigorous company culture inspired by Kent Taylor’s vision.

Starbucks (SBUX) has 10,628 company owned stores and 18,216 licensed. Personally I consider that a drug dispensary rather than a restaurant.

Wendy’s (WEN) has 7,095 restaurants worldwide. Their new CEO Kirk Tanner made some noise recently with his comments about AI order-taking and flexible pricing, which the company then walked back. It sounded kinda fun to me (what if you could get a deal at an off hour or something) and made for many a meme. Kirk Tanner seems to get in the news a lot: Wendy’s doing drone delivery was a headline on Drudge the other day. Those all seem like distractions or possibly stunts? Wendy’s big play at the moment is expanding into breakfast.

Wingstop (WING) is growing fast: 1,996 restaurants. The stock has doubled in the last year. The people love wings!

Yum Brands (YUM) with KFC, Pizza Hut, Taco Bell, and Habit Burger is on another level. They opened 4,754 new units last year.

Jack in the Box (JACK) swallowed Del Taco a few years ago. Here’s CEO Darin Harris speaking about the culture of servant leadership. I like what I hear!

New York hot dog chain Nathan’s and Chicago hot dog chain Portillo’s are both public companies, NATH and PTLO respectively. I’m not bullish on the future of hot dogs myself. If I were on the board of Nathan’s (I’m not) I’d lean into the hot dog eating contest aspect. That could be completely the wrong way to go, who knows, but they’ve got to take a swing.

I’ve never seen a Kura Sushi, but some investors appear to be optimistic about the technology-enabled Japanese sushi concept – the stock (KRUS) is up 41% this year.

Casey’s (CASY) runs some 2,500 gas station pizza joints in the Midwest. The Casey’s in Corning, Iowa was the only place to eat one Sunday night last summer. It was not bad at all! Iowan amigo Brooks tells me it’s beloved, that you should try the sausage pizza. Not much more is easily available to me on founder Donald Lamberti other than that he is in the National Sprint Car Hall of Fame. “Kind of a monopoly on many, many tiny markets”? A growing business.

Flanigan’s (BDL) is a Florida chain famed for their dolphin sandwich (don’t stress, it’s actually mahi mahi). Why it’s publicly traded doesn’t make sense to me, but there you go. I’ve never been, I collected a firsthand report or two that suggested it’s a real good time, if not necessarily Wall Street’s most ambitious concern.

Some amateur investor types love RCI, aka Rick’s (RICK), a chain of strip clubs, on the thesis that it’s kind of hard to launch a new strip club, as nobody wants ’em in their neighborhood. I’m not sure Bombshells counts as restaurants, but a publicy traded strip club joint with an expressive CEO is a noteworthy indicator.

Anyone been to a Chuy’s (CHUY)?

On May 31, 2001, then President George W. Bush’s twin daughters, Jenna Bush and Barbara Bush, were cited for using fake IDs at the Barton Springs Road Chuy’s, which put Chuy’s in the national spotlight

Next time in Austin maybe. What’s the gameplan for Chuy’s? From their recent earnings call:

As we look ahead, we will continue to do what we do best to provide our guests with fresh, made from scratch food and drinks at an incredible value. Despite weather issues across the country that has impacted the restaurant industry in January, we believe the initiatives we put in place to drive long-term sustainable top line growth and profitability has positioned us well to weather these near-term challenges.

With that, let me provide some update on our growth drivers. Starting with menu innovation. As we mentioned on our last call, we introduced our first barbell approach to the CKO platform during the fourth quarter, and we were very pleased with how well it was received by our guests. In fact, this was our second most successful Chuy’s Knockouts campaign to-date.

Following this success, we were thrilled to introduce to our guests the next CKO iteration in late January with Shrimp & Crab Enchiladas with Lobster Bisque sauce as a higher-priced CKO menu item, along with Macho Nachos and the Cheesy Pig Burrito. Again, early feedback continues to be positive as our CKOs are resonating well with both new and returning guests.

Alongside our exciting CKO offering, we recently added several new menu items to our permanent menu, including reintroducing the Appetizer Plate and adding the Burrito Bowls. If you recall, Burrito Bowls were part of our CKO platform during the second and third quarter of 2023 and this menu

etc etc. Good luck Chuy’s!

And of course, Cheesecake Factory (CAKE), much mocked, but enduring. Ate there the other day with some colleagues. You know what? My Santa Fe Salad was good. What do we think of this?:

Much lunch conversation turned on this.

CAVA is a new Mediterranean restaurant concept from the East Coast. A new one appeared here in LA. I tried it. Their operating system was not perfect (in fairness, think this is a new branch). Kinda salty?

The stock seems to excite investors, possibly because everyone is looking for “the next Chipotle.” Appears to be up 5% just today! I checked in with one of my Vibes Reporters:

i have had cava once. ok but didnt feel the need to go back

Kinda how I felt? The pita chips are fun. I just don’t think Mediterranean food will have quite the appeal of Chipotle.

Sweetgreen (SG) is a salad deal, I’ve tried that one. Somehow, I always feel gross afterwards.

On the other end of the spectrum is Cracker Barrel (CBRL) serving Southern-inspired slop to old people. Valueline reports:

Macroeconomic factors have impacted Cracker Barrel Old Country Store’s sales. Elevated inflation, though now apparently easing, has stressed the company’s customers. Many of these customers are in the 65-and-older demographic, commonly characterized as a fixed-income category. Management is working to bring in more of a younger crowd into Cracker Barrel restaurants and in-location retail shops,

Good luck guys, but this looks to me like the past, not the future:

Then again, Cracker Barrel has (had?) their loyalists:

From 1977 to 2017, married couple Ray and Wilma Yoder drove a combined total of more than 5 million miles (an average of 342 miles per day) to visit 644 Cracker Barrel locations. When the company opened their 645th restaurant, in Tualatin, Oregon, in August 2017 (on Ray Yoder’s 81st birthday), it flew the Yoders out for the grand opening and presented them with custom aprons and rocking chairs, among other gifts.[52][53]

Yoshiharu (YOSH) is a Southern California ramen concept I have yet to try. There’s also Noodles & Company (NDLS). Why is their ticker symbol not NOOD? Missed opportunity. The noodles game seems too competitive to me, talk about low margins.

But then again look at the big winners here: MCD, DPZ, CMG. Burgers, pizza, burritos. You couldn’t come up with businesses with more competition, no barriers to entry. And yet these three systematized delivery and managed quality control in such a way as to create unstoppable empires.

I began this post as I was reading Value Line’s restaurant issue and enjoying contemplating the massive scale of these restaurant chains. As an occasional restaurant consumer I can engage with these places and sense their vibe, it’s a sector I can know in a way I can’t know, say, semiconductors or industrial products. So it’s an engaging, practical and delicious topic for our continued education in business.

Restaurant Business might be the next frontier to explore. They have a daily podcast!

Growing at exactly the right pace and to exactly the right size seems like the key for restaurant stocks. On his Invest Like The Best podcast, Patrick O’Shaughnessy interviewed Capital Management’s Anne-Marie Peterson. She talked restaurants:

So restaurants are different from retail because it’s not as easy to scale. There aren’t a bunch of large cap restaurant chains unlike retail. The franchise model is pretty powerful and what Chipotle has done is pretty powerful, too. But the similarities are like real estate matters, the store experience matters. But in a tight labor market, it’s tough.

And what’s interesting about McDonald’s — I have such an affection for that company. It works everywhere. They have one concept. I think it’s 60% or 70% of their operating income is from rent. They’re a landlord. They control the real estate. The others didn’t, so that’s why they’ve endured. They had a big insight about like let’s own the real estates so our franchisees don’t get whipped around with pricing, and we can co-invest with them in the experience.

And now digitals. The mobile ordering is enhancing the productivity and reducing even those kiosks. That need for labor and in a tight labor market, it’s big. The little guys can’t invest. They have some external dynamics now that are contributing to scale. But it’s really interesting.

Rory Sutherland brought up McDonald’s automated screens on Rick Rubin’s Tetragrammaton podcast. He wondered if they might allow for customers to make certain shameful orders they feel bad about saying to a person. I’ve tried out the automated screens, they work great at getting you your junk, but they make the world a little less human.

Remember when Eric Schlosser’s book Fast Food Nation came out in 2001? Absolutely everybody was reading it. They made a movie (pretty good! Richard Linklater). Yet here we are, almost twenty five years later, eating more fast food than ever.

I was reading The Lorax to baby and it reminded me of Schlosser.

Here’s a more comprehensive list of restaurant stocks as I’ve skipped a few, notably Denny’s (DENN, slumping), Red Robin (RRGB, hopeless), El Pollo Loco (LOCO, stop trying to make citrus-marinated chicken happen), BJs, a few others.

“Treat” shops such as Krispy Kreme are beyond the scope of this post.

S

Posted: March 11, 2024 Filed under: business Leave a commentIn the book’s preface, Smil writes that most growth processes—“of organisms, artifacts, or complex systems”—can be plotted on a so-called S-shaped, or sigmoid, growth curve, meaning that the rate of change increases slowly at first, then increases rapidly, then levels off. An error that humans make with similarly predictable regularity is to assume that the nearly vertical middle segment of an S-shaped curve can continue at that angle indefinitely (the price of Dutch tulips in the seventeenth century, the price of bitcoin in the twenty-first). One of his conclusions is that the steady, unceasing economic expansion that economists and politicians dream of is not sustainable, and that the relentless pursuit of growth is environmentally disastrous. Smil has often said that he doesn’t make forecasts—“a pathetically and inexorably ever-failing endeavor on any level,” he told me—but predictions of a kind are implicit in much of his work. In “Growth” ’s coda, he writes, “Continuous material growth, based on ever greater extraction of the Earth’s inorganic and organic resources and on increased degradation of the biosphere’s finite stocks and services, is impossible”—a principle that, in various forms, animates almost all his work, beginning with his undergraduate thesis.

from The New Yorker’s profile of Vaclav Smil. I got much value from his book on natural gas, still working on How The World Really Works.

Slow lanes

Posted: January 30, 2024 Filed under: business Leave a commentEd Catmull, when president of Pixar, the animation studio, built good friction into the process of developing films such as Toy Story. “The goal isn’t efficiency, it is to make something good, or even great,” he explained to Sutton and Rao about the way his team worked through multiple versions of the original idea, improving it as the movie developed. Colette Cloosterman-van Eerd of Jumbo, a Dutch grocery store chain, saw the need to offset the drive for more efficiency with good friction. She instituted “slow lanes” that would allow checkout staff to chat to shoppers, particularly senior citizens who valued social interaction more than speed.

from a piece on Stanford BS professors Huggy Rao and Bob Sutton in Financial Times.

I also loved this idea for a column:

goddamn lunatic

Posted: December 2, 2023 Filed under: America Since 1945, business 2 CommentsOne last bit of Mungeriana, from the CNBC final interview:

BECKY QUICK: What kind of things would you recognize that they– that they were doing wrong?

CHARLIE MUNGER: Oh. They had some crazy idea. For instance, my Latin teacher was maladjusted, but one who was a devoted follower of Sigmund Freud. And I recognized that Sigmund Freud was –when I first read him when I was in high school. And, of course, it was an odd little boy whose Latin teacher is teaching him Freud. But that was – she was peculiar and so was I. And, of course, when I read – I bought the complete writings of Sigmund Freud from the area library. It was one big book. And I went through it very laboriously. And I realized he was a goddamn lunatic. And so I decided I wasn’t gonna learn that from my Latin teacher. I had some very unusual teachers. The best teacher I had in my life was Lon Fuller. Well, he was the best contracts teacher in any law school. And contracts is the best subject in every law school, at least I think it is. Because it integrates so beautifully with the new doctrine of an economics that came along with Adam Smith and all those people.

I had Dall-E generate some images of boy Charlie Munger reading the complete works of Sigmund Freud:

Horrifying.

Charlie Munger, weatherman.

Posted: November 28, 2023 Filed under: America Since 1945, business, California Leave a comment

“Like Warren, I had a considerable passion to get rich,” Munger told Roger Lowenstein for Buffett: The Making of an American Capitalist, published in 1995. “Not because I wanted Ferraris — I wanted independence. I desperately wanted it. I thought it was undignified to have to send invoices to other people.”

from Bloomberg.

Munger never stopped preaching old-fashioned virtues. Two of his favorite words were assiduity and equanimity.

He liked the first, he said in a speech in 2007, because “it means sit down on your ass until you do it.” He often said that the key to investing success was doing nothing for years, even decades, waiting to buy with “aggression” when bargains finally materialized.

He liked the second because it reflected his philosophy of investing and of life. Every investor, Munger said frequently, should be able to react with equanimity to a 50% loss in the stock market every few decades.

The Financial Times has the best obituary, noting stuff others miss like Munger’s role in funding abortion rights, here’s a link that will work for the first three lucky readers.

Munger on horse race betting, from his most famous (or second most famous?) speech:

How do you get to be one of those who is a winner—in a relative sense—instead of a loser? Here again, look at the pari-mutuel system. I had dinner last night by absolute accident with the president of Santa Anita. He says that there are two or three betters who have a credit arrangement with them, now that they have off-track betting, who are actually beating the house. They’re sending money out net after the full handle—a lot of it to Las Vegas, by the way—to people who are actually winning slightly, net, after paying the full handle. They’re that shrewd about something with as much unpredictability as horse racing. And the one thing that all those winning betters in the whole history of people who’ve beaten the pari-mutuel system have is quite simple. They bet very seldom. It’s not given to human beings to have such talent that they can just know everything about everything all the time. But it is given to human beings who work hard at it—who look and sift the world for a mispriced bet—that they can occasionally find one. And the wise ones bet heavily when the world offers them that opportunity. They bet big when they have the odds. And the rest of the time, they don’t. It’s just that simple. That is a very simple concept. And to me it’s obviously right—based on experience not only from the pari-mutuel system, but everywhere else.”

One day Warren Buffett and Charlie Munger visited the set of The Office to film a comedy video for the Berkshire Hathaway annual meeting. Everyone swarmed around Buffett but nobody really knew Munger. When the lunch break came I had the opportunity to take my plate and sit right down across from him.

From reading his Wikipedia page that morning I’d learned that Charlie Munger had been a weatherman during World War II, so I asked him about that. “It was kind of a humdrum job,” he said, modest. “A lot of people had humdrum jobs in the war.” His job was hand-drawing weather maps to predict the best times to fly planes across the Bering Strait to our Soviet allies in such a way that the engines wouldn’t ice up and kill the pilots. It seems like that might teach you something about probability and decision-making under uncertainty.

We talked about Clifton’s Cafeteria in downtown LA. He expressed admiration for that institution.

In 1931, Clinton leased a “distressed” cafeteria location at 618 South Olive Street in Los Angeles and founded what his customers referred to as “The Cafeteria of the Golden Rule”. Patrons were obliged to pay only what they felt was fair, according to a neon sign that flashed “PAY WHAT YOU WISH.” The cafeteria, at the western terminus of U.S. Route 66, was notable for serving people of all races, and was included in The Negro Motorist Green Book.

The conversation itself wasn’t that profound, but it launched me on a project of learning about more about Munger and his thinking that’s really changed my life.

“You don’t have a lot of envy.

You don’t have a lot of resentment.

You don’t overspend your income.

You stay cheerful in spite of your troubles.

(this from a guy whose first child died of leukemia).

You deal with reliable people.

And you do what you’re supposed to do.

And all these simple rules work so well to make your life better. And they’re so trite.”

His prescription is logical, he says.

“Staying cheerful” is “a wise thing to do,” Munger told Quick, adding that in order to do so, you have to let go of negative feelings.

“And can you be cheerful when you’re absolutely mired in deep hatred and resentment? Of course you can’t. So why would you take it on?” Munger said.

from 2019. (Struck by a resemblance to the mantra Liam Clancy gave Bob Dylan: “no fear, no meanness, no envy.”) He was committed to being rational, and he was witty, he expressed a lot of wisdom in a fast and punchy way. You could listen to him talk for a long time and not get bored. (And he could talk for a long time too.)

On getting the first $100,000, the hard part:

Munger holding forth in February, 2022 with a rare stock pick:

But I would argue that if I was investing money for some sovereign wealth fund or some pension fund with a 30,40, 50-year time horizon I buy Costco at the current price.

Here’s Costco vs. S&P 500 over that timeline:

(although my guy was talking 30-50 years.)

Posting about Munger has led to some interesting real life connections. The Mungerheads search out every scrap on the man. They’re interesting people to talk to, and you usually learn something

pic from the Daily Journal Co. website.

In appreciation of Munger’s life and wisdom, here are references to the man over the years at Helytimes:

Munger Speaks, 2019. On stagnation, and some life advice.

Munger and Lee Kuan Yew. There was a Confucian streak in Munger, maybe a little anti-democratic.

Buffett Bits, and Munger, from the 2020 annual meeting.

Munger and Buffett highlights from the 2021 annual meeting.

Charlie Munger Deep Cuts, my most thorough look at the guy and his wisdom (some funny ones, too, see what he says about Al Gore.

Ominous Remark from Charlie Munger, 2018.

“I’ve mellowed because I consider it counterproductive to hate as much as both parties now hate, and I have disciplined myself,” Munger said. “I now regard all politicians higher than I used to. I did that as a matter of self-preservation.” He said that he had re-read “The Decline and Fall of the Roman Empire,” and it made him “feel a lot better about the current political scene. We’re way ahead of the Romans at the end.”

That’s a pretty low bar, I pointed out.

“It’s very helpful — I suggest you try it,” Munger replied. “Politicians are never so bad that you don’t live to want them back. There will come a time when the people who hate Trump will wish that he was back

Free Samples, from 2023, a look at a commonality in Buffett-Munger businesses.

I’m All Right on That One, a few quotes from the bros of Omaha, 2023:

CHARLIE MUNGER: I used to come to the Berkshire annual meetings on coach from Los Angeles. And it was full of rich stockholders. And they would clap when I came into the coach section. I really liked that. (LAUGHTER) (APPLAUSE)

How the Chevalier de Méré met Blaise Pascal, a look at the origins of probability theory.

Obviously, you’ve got to be able to handle numbers and quantities—basic arithmetic. And the great useful model, after compound interest, is the elementary math of permutations and combinations. And that was taught in my day in the sophomore year in high school. I suppose by now in great private schools, it’s probably down to the eighth grade or so.

It’s very simple algebra. It was all worked out in the course of about one year between Pascal and Fermat. They worked it out casually in a series of letters.

More.

You know what? I wish they’d build the giant near-windowless dorm he proposed for UC Santa Barbara.

the purpose of the beehive

Posted: June 10, 2023 Filed under: business Leave a commentCOWEN: What do you think is the central insight you have about how to build that, that is otherwise under-emphasized?

GODIN: I think that Frederick Taylor’s demise is long overdue, that the purpose of a beehive is not to maximize the amount of honey we produce. The honey is a by-product of a successful beehive. That what we have is the chance to get what we want by connecting with people who have a choice about where they work, who choose to enroll with us, to avoid the false proxies of “You look like me” or “You sound like me” or “I want to have lunch with you” when we hire people, and instead dance with the people from whatever background that are going to make our project better.

When you lay it out that simply, people go, “Well, of course.” Then they go back to work in some place that demeans them and undermines them and asks them to phone it in. It just breaks my heart to see that gap.

Seth Godin talking to Tyler Cowen.

50 Cent on water

Posted: June 9, 2023 Filed under: business, water Leave a commentJust looking at things and not understanding why they’re the way they are sparked interest and ideas. I may walk down the grocery aisle, see a gallon of spring water for $2.69, and then I walk farther down, and there’s a gallon of spring water for 59 cents. And I’m like, So I wouldn’t know whether that was Poland Spring if it was in two different glasses. Yo. I want to sell water. This was before I knew Vitamin Water existed. But I knew I could charge $1.50 extra per piece and it wouldn’t even matter. I could get in the middle of that, come in at a dollar and change, and see what happens.

from this Vulture interview.

Free samples

Posted: May 22, 2023 Filed under: America Since 1945, business 1 CommentI was in See’s Candy the other day, as I am on many a weekend, and it dawned on me that two of the classic Buffett/Munger businesses, Costco and See’s Candy, are places that offer delicious free samples.

Go to a Costco and you’ll likely get a tasty snack or two, go to See’s and you’ll get whatever the day’s sample is (yesterday it was salted dark chocolate caramel).

Buffett and Munger are all about urging people to be rational, and managing their own emotions (“I can’t recall any time in the history of Berkshire that we made an emotional decision”) but a huge part of their success and what makes them interesting is their awareness that some businesses are sort of magical. They’ve got a grip on customers that’s beyond rational, that exists in the worlds of love and nostalgia and strong emotion. Buffett raving about the iphone, for instance:

If you’re an Apple user and somebody offers you $10,000, with the the only proviso [that] they’ll take away your iPhone and you’ll never be able to buy another, you’re not going to take it

If they tell you [that] if you buy another Ford motor car, they’ll give you $10,000 not to do that, [you’ll] take the $10,000 and buy a Chevy instead.

I mean, it’s a wonderful business. We can’t develop a business like that, and so we own a lot of it. And our ownership goes up over time.

Or See’s:

People had “taken a box on Valentine’s Day to some girl and she had kissed him … See’s Candies means getting kissed,” he told business-school students at the University of Florida in 1998. “If we can get that in the minds of people, we can raise prices.”

“If you give a box of See’s chocolates to your girlfriend on a first date and she kisses you … we own you,” the investor said in “Becoming Warren Buffett,” an HBO documentary.

(That U Florida interview is one of my favorite Buffett texts, you can see not just the sunny old grandpa but the rapacious capitalist).

There is an accounting term that attempts to quantify some of this, goodwill, but this quality is not measurable in any exact way. In Munger’s famous talk on The Psychology of Human Misjudgment, he talks about how he didn’t learn about any of this at Caltech or Harvard Law School. Being rational is wise, even a moral duty as Munger often says, but you’ll miss out on human decisionmaking if you don’t look for and acknowledge the power of essentially magical forces at work.

The gap between rationality and the way people actually behave due to romantic attachments, sentimentality, brand loyalty, etc is a source of humor, as well as an opportunity for price increases. Buffett and Munger seem to see both.

One example I can think of where free samples didn’t work: the teriyaki place at the mall. Did you have these? At the mall food court the kid at the teriyaki place would often have a plate of free samples. Yet the one time I tried a full plate it was kind of repulsive. I didn’t finish. Too sweet or something, or just not good at scale.

Coke has no taste memory. You can drink one of these at 9 o’clock, 11 o’clock, 3 o’clock in the afternoon, 5 o’clock. The one at 5 o’clock will taste just as good to you as the one you drank early in the morning. You can’t do that with cream soda, root beer, orange, grape, you name it. All of those things accumulate on you. Most foods and beverages accumulate on you — you get sick of them after a while. There is no taste memory to cola.

So says Buffett, perhaps related to “the teriyaki problem.”

Maybe the free sample method only works with a quality product. Sometimes the samples at Costco are bad. Remember when they used to give a sample at Trader Joe’s? Covid has killed that I guess. It worked on me.

Giving out free samples, in both See’s and Costco’s case, represents a strong investment on serving customers. Giving out free samples is a pain in the butt. A business that has the abundance to consistently deliver is probably confident and well-managed. Is this blog a form of free samples?

I’m all right on that one

Posted: May 11, 2023 Filed under: America Since 1945, business Leave a comment

And there used to be a politician in Nebraska, and if you asked him some really tough question like, you know, how do you stand on abortion, he would look you right in the eye and he’d say, “I’m all right on that one.” And then he’d move next.

very Warren Buffett joke from Warren Buffett.

You know, Tom Murphy, the first time I met him, said two things to me. He said, “You can always tell someone to go to hell tomorrow.” Well, that was great advice then. And think of what great advice it is when you can sit down at a computer and screw your life up forever by telling somebody to go to hell, or something else, in 30 seconds. And you can’t erase it. …

And then the other general piece of advice, I’ve never known anybody that was basically kind that died without friends. And I’ve known plenty of people with money that have died without friends, including their family. But I’ve never known anybody, and you know, I’ve seen a few people, including Tom Murphy Sr. and maybe Jr., who’s here, (LAUGH) but certainly his dad, I never saw him, I watched him for 50 years, I never saw him do an unkind act.

on fun:

And we had as much fun out of deals that didn’t work in a certain sense as the ones that did work. I mean, if you knew you were going to play golf and you were going to hit a hole in one on every hole, you just hit the ball, and it went in the hole that was 300 yards away, or 400 yards away, nobody would play golf.

I mean, part of the fun of the game is the fact that you hit them to the woods. And sometimes you get them out, and sometimes you don’t.

So, we are in the perfect sort of game. And we both enjoy it. And we have a lot of fun together. And we don’t have to do anything we don’t really believe in doing.

On See’s:

And it has limited magic in sort of the adjacent West. It’s gravitational, almost. And then you get to the East. And incidentally, in the East, people prefer dark chocolate to milk chocolate. In the West, people prefer milk chocolate to dark. In the East, you can sell miniatures, and dark — in the West —

I mean, there’s all kinds of crazy things in the world that consumers do.

Talking about Netjets:

CHARLIE MUNGER: I used to come to the Berkshire annual meetings on coach from Los Angeles. And it was full of rich stockholders. And they would clap when I came into the coach section. I really liked that. (LAUGHTER) (APPLAUSE)

(he doesn’t fly that way anymore)

from this CNBC transcript of the afternoon session of the annual meeting. I couldn’t find a transcript of the morning session.

Tax facts from Uncle Warren

Posted: February 25, 2023 Filed under: business Leave a comment

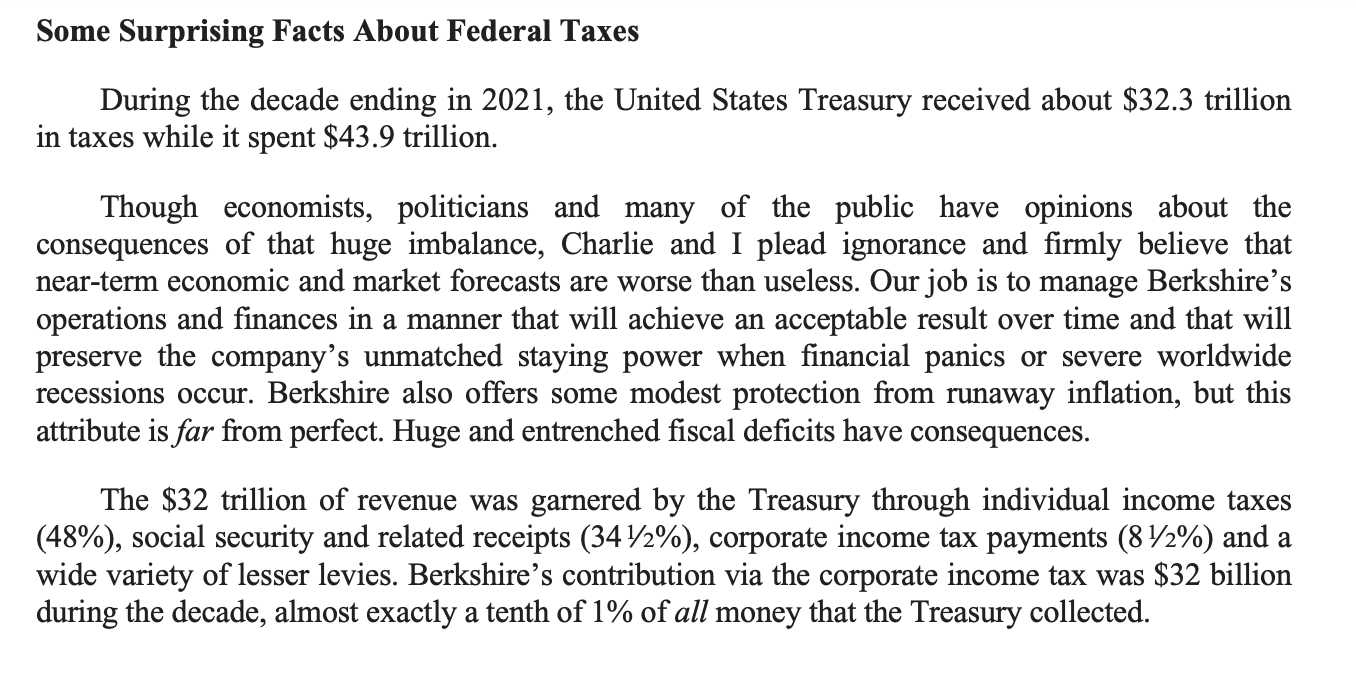

from the Berkshire Hathaway annual letter.

If you prefer Jimmy Buffett, we have that covered too.

Coins

Posted: November 7, 2022 Filed under: business, money Leave a comment

say what you will about Queen Elizabeth she looks good on a coin. I wonder if some of the turbulence in UK markets of late have to do with the fact that Steady Grandma will no longer be on the money, now it is Weird Son.

French coin picked up most likely in Tahiti

The Euro’s kind of ominous, no?

Who runs Bartertown?

Posted: July 18, 2022 Filed under: America Since 1945, business, politics Leave a commentWhen he gets to Bartertown, Max is taken up in the tower to meet Aunty (Tina Turner). She tells him she wants him to kill somebody. Who? Master Blaster.

Master is a little gnome who rides around on the giant Blaster. Aunty explains that the energy to run the lights and electricity of Bartertown comes from the underworld, a horrible factory-like place where pig shit generates methane.

Max goes down to the underworld under the guise of a pig-shit shoveler. While there, he meets Master Blaster, who is determined to show him who really runs Bartertown. Master Blaster turns off the methane to Bartertown. Everything goes dark. Master Blaster calls up to Aunty. His demand to turn the methane back on is that she answer the question: Who run Bartertown? Reluctantly, she answers: Master Blaster. He makes her say it publicly, over the PA system. Who run Bartertown? Master Blaster. Once she’s said this he smiles and turns the methane back on.

That’s all pretty early in the movie, we haven’t even gotten inside the Thunderdome yet. And since the movie is called Mad Max Beyond Thunderdome, we know we’re barely getting started.

Market research

Posted: July 10, 2022 Filed under: business Leave a commentMy data-driven advice for getting rich for someone with good analytical skills and deep experience in a field is to start a market research business. Use your specialized knowledge in the field to write up reports; sell them widely and charge a fortune to your contacts in the field. I have estimated that more than 10 percent of owners of market research businesses are in the top 0.1 percent.

from this NY Times op-ed, “The Rich Are Not Who We Think They Are,” by Seth Stephens-Davidowitz.

Intrigued, I Googled “how to start a market research business” and found:

There are a number of market researchers out there fighting for the same business you are. Consider your own business the firm’s first client. What does your target audience respond most to? Build a marketing strategy around that. Highlight your strengths through the use of existing contacts, networking, and cold calling. Get involved by attending conferences. Offer to speak at a conference or become a committee member.

Bold is mine, that’s brilliant. It does sound like a lot of work though. But, Stephens-Davidowitz tells us:

A study of thousands of millionaires led by researchers at Harvard Business School did find a gain in happiness that kicks in when people’s net worth rises above $8 million. But the effect was small: A net worth of $8 million offers a boost of happiness that is roughly half as large as the happiness boost from being married.

That sounds good?

Mining News

Posted: June 26, 2022 Filed under: business Leave a comment

forget what search or series of searches led to me being hit with these ads. Don’t mind it.

An egg a day

Posted: June 25, 2022 Filed under: business, food Leave a commentJoe Weisenthal Tracey Alloway interview their colleague Tim Culpan about FoxConn and founder Terry Guo.

And so one of the first things Terry Guo did was he said, okay, I want all of my workers to eat well. So every single one of them would get an egg a day, so they could get a bit of protein. That was kind of a bit of a way out idea at the time. This was, just to be clear, this was in the eighties, seventies and eighties, seventies and eighties. And so Terry Guo is not an electronics guy. Most people in the tech industry have a tech background, they have an electronics background, maybe electronic engineering, Terry Guo studied at a maritime college in Northern Taiwan. So he really studied shipping and logistics, and then he moved into plastics. So his kind of opening business was plastic injection molding. And if you think of Taiwan in the seventies and eighties, it was known, as you know, ‘Made in Taiwan,’ cheap plastic toys, Barbie dolls, and everything else was made in Taiwan.

That’s my bold.

Some of the history of the world:

Joe: (13:44)

How did Apple find Foxconn?Tim: (13:48)

Well when Steve Jobs came back, as we all know, the company was in trouble, they, Apple was actually making their computers — like physically making them in California, but over a period of time, many companies, you know, Michael Dell and Hewlett Packard, Compaq, and others were starting to outsource to Asia. And at some point during that period of time, Tim Cook, who was operating officer at the time, he’d not yet become CEO, would’ve discovered Foxconn and realize that, you know, these guys make the components. We should probably get to know them. And they really jumped into bed deeply when the iPod came out in the early 2000s.

Harsh

Posted: June 14, 2022 Filed under: business 1 CommentThis morning, Coinbase CEO Brian Armstrong announced his firm will lay off roughly 18% of staff in a less-than ceremonious manner – via automatic removal of access to the office email server

wow. Cold. Almost Daily Grant’s continues:

On the bright side, the founder will be able to mull those fast-changing circumstances in style. From the Jan. 3 edition of The Wall Street Journal:

Coinbase Chief Executive Officer Brian Armstrong is the buyer of a $133 million Los Angeles estate, according to people familiar with the deal. The transaction, which closed in December, is one of the priciest single-family home sales ever completed in the L.A. area.

Is it a bad sign that some of the best daily / column comedy writing is coming from the financial world? Matt Levine’s Money Stuff is unstoppable, Joe Weisenthal, Terminal Value…

The price of hay

Posted: June 13, 2022 Filed under: America Since 1945, art history, business Leave a comment

A friend of ours who runs a horse barn told me the price of hay is up $5 a bale, from $27 to $32.

(I know what you’re thinking, that’s a lot for hay, but trust me, these horses are getting primo stuff.)

(painting is Rhode Island Shore by Martin Johnson Heade, at LACMA, not on display last I was there).

The Price of Gas

Posted: June 12, 2022 Filed under: America Since 1945, business, the California Condition Leave a comment

It’s so high! How can people do anything? Yet shouldn’t we want the price of gas to be high, so we don’t cook up the planet quite as fast? Though, won’t the high prices cause estimates and spreadsheets and algorithms across the oil and gas companies to be adjusted? When the calculations are revised, it suddenly makes sense to drill more and deeper and in crazier ways in more chaotic countries? They’ll capitalize new and more projects, dredging up our oil faster than ever.

Is this merely the boom and bust cycle we all must toil under, written many times over in the history of every boomtown and oil craze? From Nantucket to Houston to the Bakken to Bakersfield to Alaska we are told this story. Above LA looms the Getty, named for a man whose father left Minnesota for a boom in Bartlesville, Oklahoma. The son took the lesson and was early in on Saudi Arabia. To get to the Getty from here you’d have to cross Doheny, he of Teapot Dome. But look, you saw the oil wells when you came in from the airport (in a car), and if you looked out the window of your plane as you landed at LAX you saw the diesel tankers and maybe even an oil tanker filling up at the offshore spigot. You get the idea.

Not so long ago I watched the documentary version of The Prize in small chunks, just before bed. Though the content can be bracing it is soothingly narrated by Donald Sutherland, and there is something relaxing about seeing how the pieces fit together. Finding the doc compelling I read Daniel Yergin’s original book, which is full of great characters and strange scenes:

In early March 1983 the oil ministers and their retinues hurriedly convened, ironically in London, the home court of their leading non-OPEC competitor, Great Britain. They met at the Intercontinental Hotel at Hyde Park Corner, for what turned out to be twelve interminable, frustrating days – an experience that would leave some of them with an allergic reaction whenever, in future years, they set foot inside the hotel.

and:

Later in the day, Silva Herzog was glumly eating a hamburger at the Mexican embassy, preparing to leave, when a call came from the United States Treasury saying that the $100 million fee had been rescinded. The Americans could not risk a collapse. Who knew what the effects would be on Monday? And with that, the Mexican Weekend concluded, with the first part of the emergency package now in place.

Some takeaways of value:

- it’s not just the getting of the oil. It’s the refining. Rockefeller controlled the refining, and the shipping, and eventually everything

- one of Rockefeller’s killer qualities: he was a visionary accountant. Can there be such a thing? Yes. Rockefeller.

- The Great War, later World War One, was a gamechange for oil. Railroads had been key in the US Civil War, but in World War One, the tank and the truck, oil powered vehicles, proved to be the crucial transport. Churchill, head of the Admiralty at the time, switched the Royal Navy to oil from coal. At the end of the war, the destruction of the Ottoman Empire left the British and French in control of oil fields in Mesopotamia.

- both on the Eastern Front and in the Pacific in World War Two, oil was the key strategic factor. Really everywhere, but those offer clear examples. Decisions on how to invade the Soviet Union were based on gaining control of oil fields before the German forces ran out of oil. The Japanese navy’s decisions were bounded by limits on oil. The fleet had to be stationed near Singapore. The “Marianas turkey shoot” was a result of decisions made based on saving oil. There was not enough oil not only for active operations, but for pilot training.

How about this?:

When [J. Paul] Getty died in 1976, age eighty-three, the eulogy at his funeral was delivered by the Duke of Bedford. “When I think of Paul,” said the Duke, “I think of money.”

Many people and groups of people have attempted to control oil, but it’s unpredictable. Sometimes the board gets reshuffled: North Sea oil fields, Saudi, Alaska. The North Sea oil fields saved the UK economy. Or did it ruin the UK economy? It saved Margaret Thatcher. You can’t send ships and helicopters to the coast of Argentina if you don’t have oil.

Look how rich Norway is. It doesn’t have to be this way, Norway used to be poor, that’s why Rose on Golden Girls is from St. Olaf.

Obama’s presidency coincided with a huge boom in US oil extraction. Is “coincided” the right word? Was it a coincidence? What’s at work here?

A character worth some study: Marcus Samuel. (Shell, the first oil tanker, Lord Mayor of London).

It was called Shell because his Iraqi Jewish family used to import and sell seashells. (That’s the story, anyway.)

Here’s a solid summary of The Prize.

Recall that Moby-Dick is about the oil business, and Ahab like Daniel Plainview is an oilman.

Tom Murphy

Posted: June 10, 2022 Filed under: business Leave a commentMr. Murphy clearly wanted to grow the size of Capital Cities, but he never lost sight of the fact that growth through acquisition only creates value if it can be accomplished at sensible prices, nicely encapsulated in this quote:

“The goal is not to have the longest train, but to arrive at the station first using the least fuel.”

from this Rational Reflections post.

I am in a game

Posted: April 18, 2022 Filed under: business Leave a comment

the game is very very easy if you have the right lessons in your mind.

Buffett says that to succeed at the game you need an IQ of about 120, but more than that is a hinderance.

Nothing shocking in Warren Buffett’s interview with Charlie Rose if you are a Buffett student. He drinks a Coke. That this interview exists is perhaps the most interesting thing: Charlie Rose is back? In this form? It’s not shot like Charlie’s PBS show.

Could this room be more generic?

Warren:

I think about what the company’s gonna be worth in 10-12 years.

and:

most of them [Berkshire investors] give it away when they get through

What does “get through” mean here? Die?

Buffett mentions pitching some doctors at a place called The Hilltop House in Omaha. Sadly it no longer exists, I find this photo of it on the post “I Wish I Could Have Gone To: Hilltop House” on MyOmahaObsession and I share the sentiment.